In the current fiscal landscape of 2026, health insurance has transcended its status as a secondary employee perk to become the most significant—and often the most burdensome—expense in a standard corporate benefits package. As business owners and human resource departments navigate a post-inflationary economy, the primary question dominating executive boardrooms is no longer whether to offer health coverage, but how to sustain it. Driven by a confluence of rising hospital operational costs, a surge in chronic health conditions among the workforce, and an unprecedented demand for high-cost specialty medications, employer healthcare expenditures have maintained a steady upward trajectory over the last decade. This financial pressure is occurring simultaneously with a tightening labor market where health benefits remain the ultimate tool for talent acquisition and retention.

The Financial Reality of Group Health Insurance in 2026

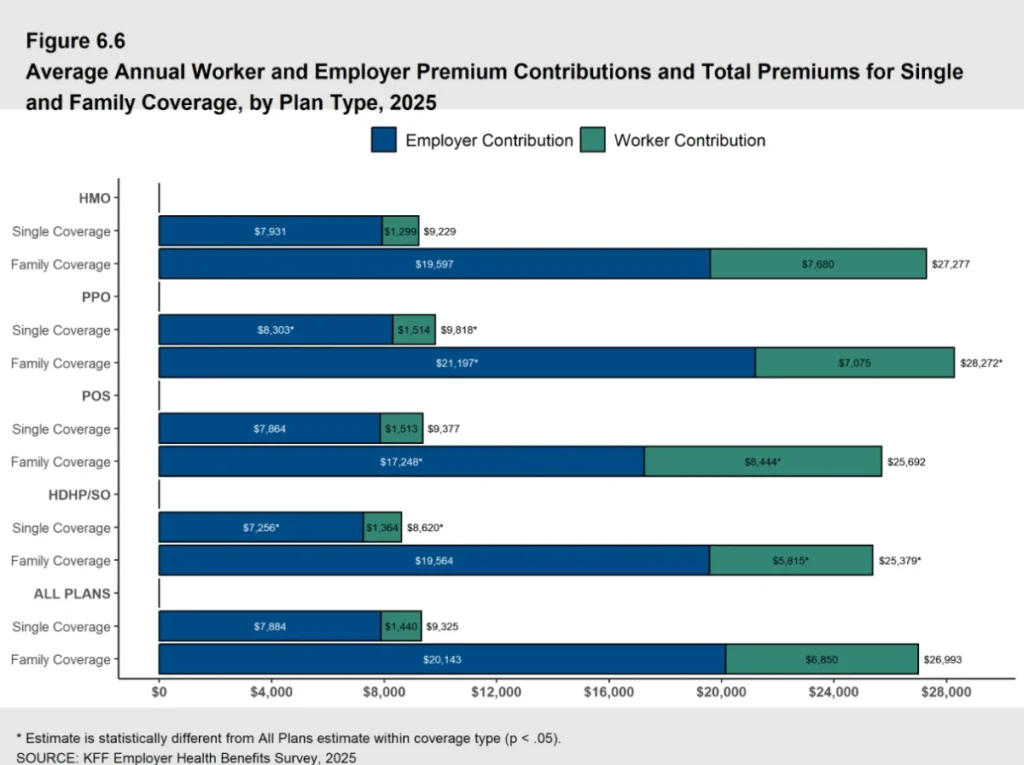

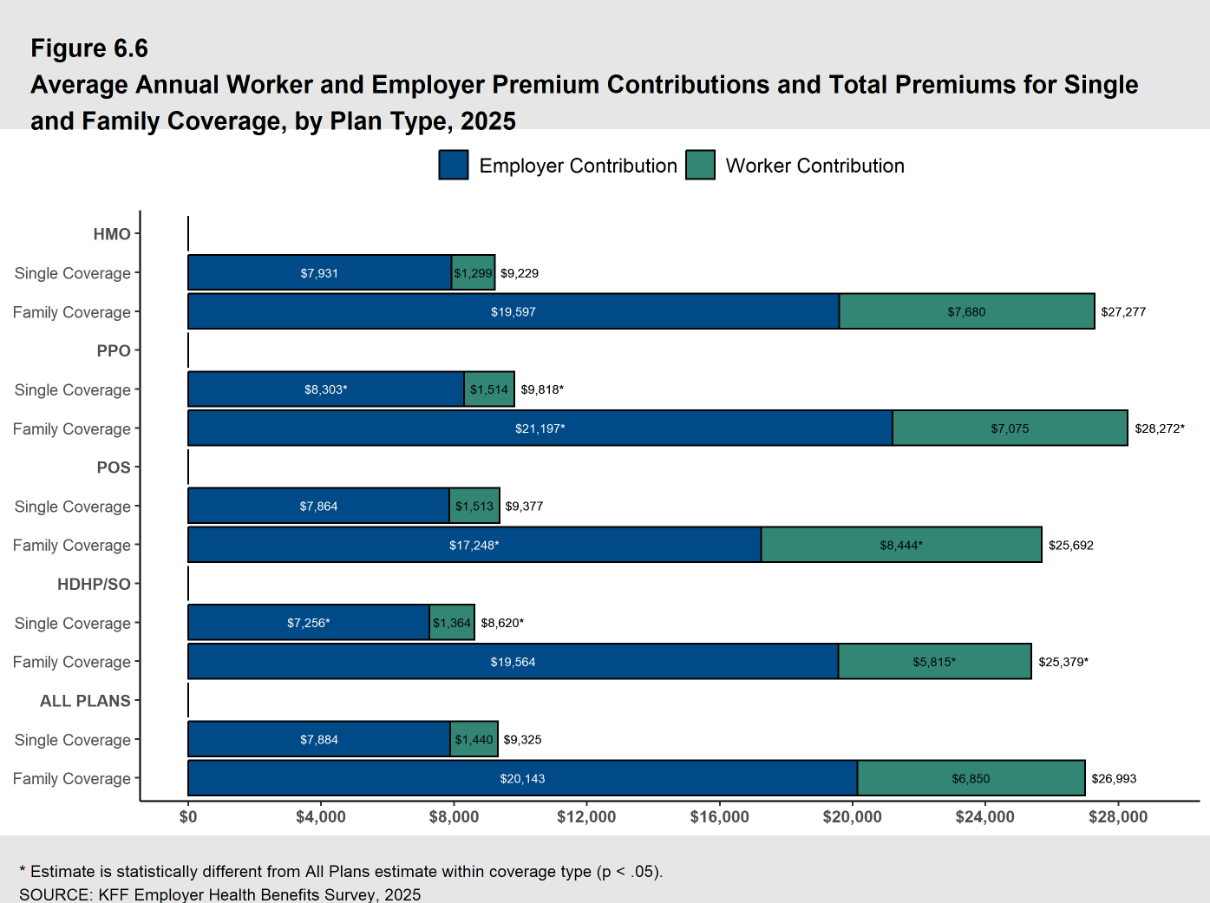

According to the 2025 Employer Health Benefits Survey conducted by KFF, the benchmark for traditional group health insurance has reached new heights. The average annual cost of employer-sponsored health insurance premiums per employee now stands at $26,993 for family coverage and $9,325 for single coverage. These figures represent a significant milestone in the cost of labor, reflecting a decade of compounded annual growth. While specific premiums vary based on the insurance carrier, the size of the organization, and the geographic location of the workforce, the trend is universally upward.

Traditional group health insurance typically falls into two categories: fully-insured and self-funded plans. In a fully-insured model, the employer pays a fixed premium to an insurance carrier, which then assumes the financial risk of medical claims. While this offers budget predictability, it often involves rigid "one-size-fits-all" structures and mandatory participation requirements that can be difficult for smaller enterprises to satisfy. Conversely, self-funded plans involve the employer directly covering the medical expenses of their employees. While this avoids the overhead of insurance premiums, it exposes the company to the volatility of high-cost medical claims, necessitating the purchase of stop-loss insurance to mitigate catastrophic financial risk.

A Decade of Growth: The Chronology of Healthcare Inflation

To understand the current crisis, one must look at the historical progression of premium costs. The average cost of family premiums has increased by approximately 26% over the last five years and a staggering 47% over the previous ten years. In 2016, the cost of covering a family was significantly more manageable; however, the intervening decade saw several systemic shifts.

The period between 2020 and 2023 introduced significant volatility due to the global pandemic, which initially saw a dip in elective procedures followed by a massive surge in healthcare utilization and labor costs within the medical sector. By 2024, the "catch-up" effect of deferred care combined with the introduction of expensive new drug classes—particularly GLP-1 agonists for weight loss and diabetes—began to drive premiums higher. By 2026, industry analysts from PwC’s Health Research Institute have noted that healthcare cost increases have stabilized at a high plateau, with average increases remaining at 8.5% for group insurance plans and 7.5% for the individual market. This represents a 3% acceleration in the growth rate compared to 2022.

The Employer-Employee Cost-Sharing Dynamic

Despite the rising costs, employers continue to shoulder the majority of the financial burden to remain competitive in the talent market. In 2025, the average employer contribution toward group health insurance premiums was 75% for family coverage and 85% for single plans. In practical terms, this means employers are paying an average of $20,143 annually for family policies and $7,884 for single coverage per employee.

For the employee, the remaining portion of the premium is typically deducted from their gross pay on a pre-tax basis. In 2025, the average employee contribution was $6,850 annually for family coverage and $1,440 for single coverage. While the employer covers the lion’s share, the increasing cost to the employee is not negligible. As premiums rise, many employees find their net take-home pay stagnating, leading to increased pressure on employers to provide higher wage increases or more efficient benefit structures.

Factors Driving the 2026 Cost Surge

Several underlying factors contribute to the persistent rise in premiums. Understanding these variables is essential for organizations attempting to forecast their long-term financial health.

- Specialty Pharmacy and Biotechnology: The development of gene therapies and advanced specialty medications has revolutionized treatment for chronic diseases but at a massive price point. Some treatments now cost hundreds of thousands of dollars per patient, which is factored into the collective risk pool of group plans.

- Hospital Consolidation: Increased merger and acquisition activity among hospital systems has reduced competition in many regional markets. Data suggests that in markets dominated by a single large healthcare system, the cost of services is significantly higher than in competitive markets.

- Chronic Disease Management: The prevalence of chronic conditions such as hypertension, diabetes, and obesity in the American workforce continues to climb. These conditions require ongoing management and high utilization of primary and specialist care.

- Labor Shortages in Healthcare: A shortage of nursing staff and specialized clinicians has forced medical providers to increase wages, costs which are ultimately passed down to insurers and employers.

The Strategic Importance of Health Benefits for Retention

While the financial data might tempt some business owners to forgo offering health insurance, the labor market implications of such a move are often catastrophic. A PeopleKeep survey indicates that 92% of employees rank health coverage as their most valued benefit. In an era where "quiet quitting" and high turnover rates plague the corporate world, health insurance serves as the primary "sticky" benefit that keeps talent within an organization.

Organizations that fail to offer competitive health benefits struggle with significantly higher recruitment costs. The expense of losing a seasoned employee—often estimated at 1.5 to 2 times their annual salary—frequently outweighs the annual cost of providing health insurance. Consequently, the challenge for modern employers is not whether to provide the benefit, but how to do so without compromising the company’s bottom line.

Innovations in Benefit Design: The Rise of HRAs

In response to the unsustainable trajectory of traditional group plans, many organizations are pivoting toward Health Reimbursement Arrangements (HRAs). An HRA is a tax-advantaged account funded by the employer to reimburse employees for qualified medical expenses and, in certain models, individual insurance premiums.

The ICHRA and QSEHRA Models

The Individual Coverage HRA (ICHRA) and the Qualified Small Employer HRA (QSEHRA) have emerged as the primary alternatives to traditional group health insurance. The QSEHRA, established by the 21st Century Cures Act, allows small businesses with fewer than 50 full-time equivalent employees to provide tax-free reimbursements for medical expenses.

The ICHRA, which is available to employers of any size, offers even greater flexibility. It allows businesses to define different allowance amounts based on employee classes (e.g., full-time vs. part-time) and enables employees to shop for their own health insurance on the individual market. This "defined contribution" model gives employers absolute control over their budget while providing employees with the freedom to choose a plan that fits their specific medical needs.

The Group Coverage HRA (GCHRA)

For employers who wish to maintain a traditional group plan but want to mitigate the impact of high deductibles, the Group Coverage HRA (GCHRA) serves as an integrated supplement. By switching to a lower-premium, high-deductible health plan (HDHP) and using a GCHRA to cover employees’ out-of-pocket costs (such as deductibles and copays), employers can often reduce their total spend while maintaining a high level of coverage for their staff.

The Role of Health Stipends and Tax Implications

For some organizations, particularly those with employees who qualify for federal premium tax credits, a health insurance stipend may be a more appropriate solution. Unlike HRAs, stipends are essentially additional wages added to an employee’s paycheck. They are highly flexible and have fewer regulatory hurdles than formal health plans.

However, stipends come with a distinct disadvantage: they are taxable. Employers must report stipend contributions as income on W-2 forms, and they do not satisfy the Affordable Care Act’s (ACA) employer mandate for Applicable Large Employers (ALEs). Furthermore, while an HRA is tax-deductible for the employer and tax-free for the employee, a stipend is subject to payroll and income taxes, reducing the overall "buying power" of the benefit.

Broader Impact and Future Implications

As we look toward the remainder of 2026 and into 2027, the shift toward personalized, portable health benefits is expected to accelerate. The traditional model of an employer choosing a single plan for a diverse workforce is increasingly viewed as an outdated relic of the 20th-century economy.

The broader economic implication is a move toward "consumer-driven healthcare," where employees are empowered to act as savvy consumers of medical services. By utilizing HRAs and telemedicine options—which many employers now include as low-cost add-ons to encourage early intervention—organizations are attempting to bend the cost curve.

Ultimately, the escalating cost of healthcare is forcing a fundamental redesign of the American employment contract. Employers are moving away from being "purchasers" of healthcare and toward being "enablers" of healthcare. For the modern business, success in 2026 requires a delicate balance between fiscal responsibility and a genuine commitment to employee well-being. Those who master this balance will not only survive the rising costs but will thrive by attracting the best talent in an increasingly competitive global market.