The landscape of corporate benefits in the United States has reached a critical inflection point as 2026 begins, with health insurance remaining the most significant and volatile expense for employers. According to the latest industry data, the cost of providing medical coverage has transitioned from a standard business expense to a primary strategic challenge. Driven by a confluence of rising hospital operational costs, an aging workforce with chronic conditions, and an unprecedented surge in demand for high-cost specialty medications, employer healthcare expenditures have maintained a steady upward trajectory for more than a decade. For business owners and human resource executives, the central question has shifted from whether to offer benefits to how to sustain them as costs per employee reach historic highs.

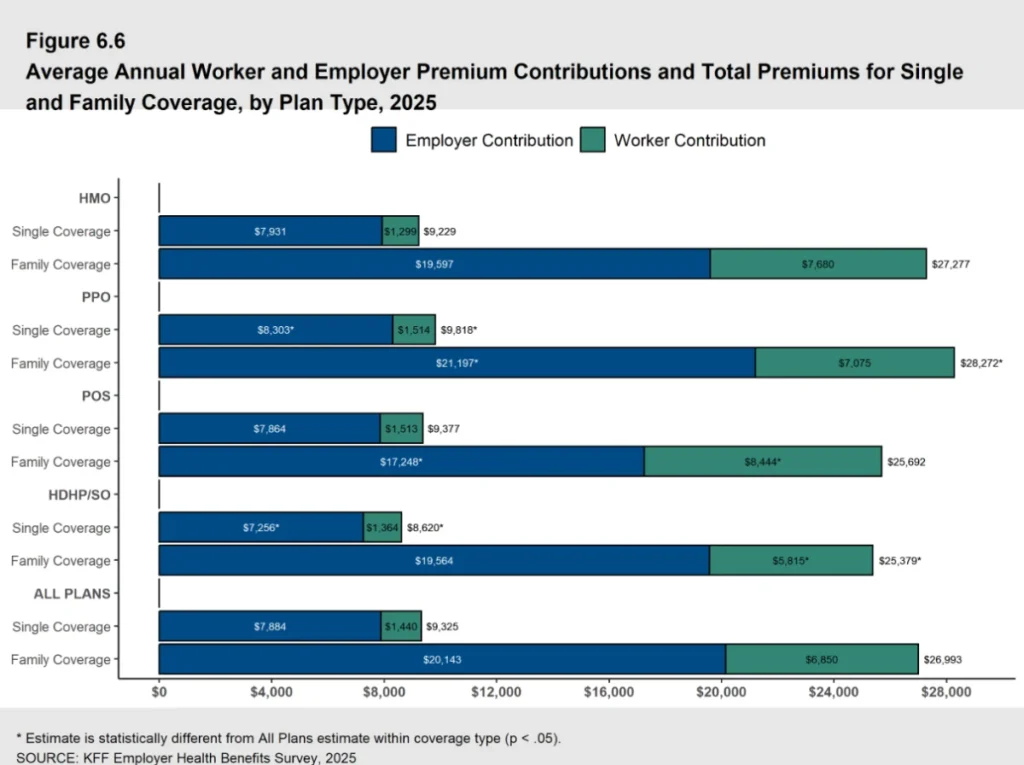

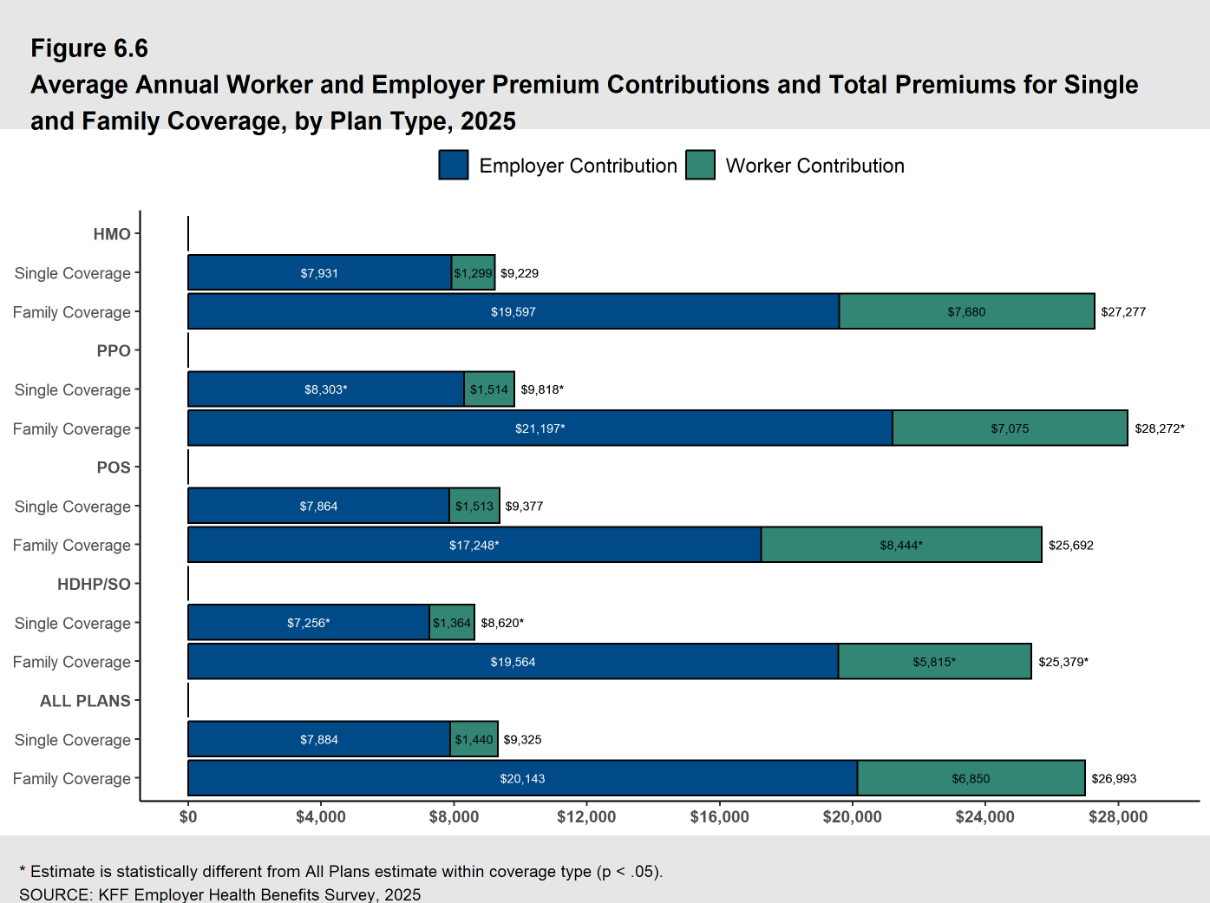

Recent findings from the KFF 2025 Employer Health Benefits Survey indicate that the average annual cost of employer-sponsored health insurance premiums has reached $26,993 for family coverage and $9,325 for single coverage. These figures represent a substantial financial commitment that continues to outpace general inflation. Despite the high price tag, the necessity of these benefits remains undisputed in the labor market. A PeopleKeep survey highlights that 92% of employees rank health insurance as their most valued benefit, suggesting that organizations attempting to forgo coverage to protect their bottom line may face severe repercussions in employee retention and recruitment.

The Financial Architecture of Group Health Insurance

To understand the current economic pressure on businesses, it is essential to distinguish between the two primary models of group health insurance: fully insured and self-funded plans. In a fully insured model, the employer pays a fixed premium to an insurance carrier. The carrier assumes the financial risk of medical claims, but in exchange, the employer often faces high administrative overhead and a "one-size-fits-all" benefit structure that may not align with a diverse workforce.

Conversely, self-funded plans involve the employer taking on the direct responsibility for employee medical expenses. While this removes the profit margin of the insurance carrier and avoids certain premium taxes, it exposes the company to the risk of catastrophic claims. Many mid-sized and large organizations mitigate this risk through stop-loss insurance policies, but the fundamental responsibility for the claims remains with the business. In 2025 and 2026, the trend toward self-funding has accelerated as companies seek more granular control over their data and spending, yet the underlying costs of care continue to rise regardless of the funding mechanism.

A Decade of Rising Costs: A Chronological Perspective

The current pricing environment is the result of a long-term trend characterized by compounding annual increases. A retrospective analysis reveals that the average family premium has increased by 26% over the last five years and a staggering 47% over the last decade.

- 2015–2019: Steady Incrementalism: During this period, healthcare costs rose at a relatively predictable rate of 3% to 5% annually. The focus was largely on the implementation of the Affordable Care Act (ACA) and the transition to electronic health records.

- 2020–2022: Pandemic Volatility: The COVID-19 pandemic introduced extreme fluctuations. While total spending temporarily dipped due to the cancellation of elective procedures in 2020, it rebounded sharply as "deferred care" returned to the system in late 2021 and 2022.

- 2023–2025: Inflationary Pressures: Post-pandemic inflation hit the healthcare sector with a lag. Labor shortages in nursing and specialized medicine forced hospitals to increase wages, which were subsequently passed on to insurers and employers through negotiated rate hikes.

- 2026: The Specialty Drug Surge: The current year is defined by the impact of specialty medications, particularly GLP-1 agonists for weight loss and advanced gene therapies. PwC’s Health Research Institute reports that healthcare cost increases have held at 8.5% for group plans in 2026, a 3% increase in the growth rate since 2022.

Supporting Data: Breakdown of Employer and Employee Contributions

The financial burden of these premiums is shared between the organization and the workforce, though the ratio has remained relatively stable despite the rising totals. In 2025, employers contributed an average of 75% toward family coverage and 85% toward single plans. In dollar amounts, this equates to an annual employer contribution of $20,143 for family policies and $7,884 for single coverage per employee.

Employees, meanwhile, are feeling the squeeze on their take-home pay. The average worker contribution for 2025 stood at $6,850 annually for family coverage and $1,440 for single coverage. These contributions are typically processed via pre-tax payroll deductions, providing some tax relief, but the absolute cost remains a significant portion of the average household budget. Market analysts note that as premiums rise, many employers are forced to choose between increasing the employee’s share of the premium or moving toward high-deductible health plans (HDHPs) to keep the monthly costs manageable.

Primary Drivers of Healthcare Inflation in 2026

Several systemic factors contribute to the persistent rise in premiums. Understanding these drivers is essential for any business attempting to forecast future benefit budgets.

- Hospital and Provider Consolidation: As hospital systems merge, their bargaining power with insurance companies increases, leading to higher negotiated rates for services.

- Chronic Condition Management: The prevalence of chronic diseases such as diabetes, hypertension, and obesity continues to rise. These conditions require long-term, expensive management and are a primary driver of high-cost claims.

- Specialty Pharmaceuticals: The "pharmacy spend" now accounts for a larger percentage of total healthcare costs than ever before. New biotech drugs often cost tens of thousands of dollars per dose, and their inclusion in standard formularies has a direct impact on group rates.

- Labor Costs in Healthcare: The healthcare sector continues to grapple with a shortage of skilled clinicians. To maintain staffing levels, facilities have increased compensation, which translates to higher costs for medical procedures.

The Strategic Shift: Health Reimbursement Arrangements (HRAs)

As traditional group insurance becomes financially untenable for many small and mid-sized enterprises, a significant shift toward "defined contribution" models has emerged. Health Reimbursement Arrangements (HRAs) allow employers to move away from picking a specific plan and instead provide employees with a tax-free allowance to purchase their own coverage.

The Qualified Small Employer HRA (QSEHRA)

Created by the 21st Century Cures Act, the QSEHRA is designed specifically for businesses with fewer than 50 full-time equivalent employees. It allows these smaller organizations to offer a formal health benefit without the administrative complexity or minimum participation requirements of a group plan.

The Individual Coverage HRA (ICHRA)

The ICHRA, introduced in 2020, expanded the HRA concept to businesses of all sizes. It offers unparalleled flexibility, allowing employers to scale allowances based on employee classes (e.g., full-time vs. part-time, or by geographic location). This model provides the employer with total budget predictability, as they decide exactly how much they are willing to contribute, leaving the employee to choose a plan from the individual market that fits their specific healthcare needs.

The Group Coverage HRA (GCHRA)

Also known as an integrated HRA, this is used in tandem with a traditional group plan. Often, an employer will switch to a lower-cost, high-deductible plan and then use a GCHRA to reimburse employees for out-of-pocket costs like deductibles and copays. This strategy helps mitigate the impact of premium hikes while maintaining a traditional insurance structure.

Official Responses and Industry Analysis

Industry stakeholders have voiced growing concern over the sustainability of the current model. Benefits consultants argue that the traditional group market is failing to provide the customization required by a modern, often remote or hybrid, workforce. "The ‘one-size-fits-all’ approach of 20th-century group insurance is increasingly incompatible with the diverse needs of today’s employees," says one benefits strategist. "We are seeing a massive migration toward HRAs because they decouple the employer’s budget from the insurer’s rate hikes."

From a regulatory standpoint, Applicable Large Employers (ALEs)—those with 50 or more full-time employees—must remain vigilant regarding the ACA’s employer mandate. To satisfy the mandate, the coverage offered must be considered "affordable" and provide "minimum value." HRAs like the ICHRA can be used to satisfy these requirements, provided the allowance is sufficient to allow the employee to purchase a silver-level plan on the exchange for a certain percentage of their household income.

The Role of Health Stipends and Tax Implications

For organizations that find even HRAs too restrictive, health stipends have become a popular alternative. Stipends are essentially additional wages designated for healthcare expenses. Unlike HRAs, stipends are taxable income and do not satisfy the ACA employer mandate for ALEs. However, they offer the highest level of flexibility and are often used by very small startups or as a supplement for employees who qualify for premium tax credits on the health insurance marketplace.

The tax-free nature of HRAs remains their strongest selling point. For the employer, reimbursements are tax-deductible and exempt from payroll taxes. For the employee, the funds are free from income tax, provided they maintain minimum essential coverage (MEC). This tax efficiency often makes the HRA a more cost-effective tool than a simple salary increase or a taxable stipend.

Broader Impact and Implications for the Future

The escalating cost of healthcare is not merely a line item on a balance sheet; it is a factor that influences the very structure of the American economy. As costs rise, businesses are forced to reconsider their expansion plans, wage increases, and investment in innovation.

The "retailization" of healthcare—where employees act as consumers of their own health plans through models like the ICHRA—is expected to grow. By 2030, analysts predict that defined contribution health benefits could become the standard for small and mid-market companies, mirroring the shift from defined-benefit pensions to 401(k) plans seen in previous decades.

In conclusion, while the cost of health insurance in 2026 presents a daunting challenge, the emergence of flexible, tax-advantaged reimbursement models provides a path forward. Employers who proactively transition from being "buyers of insurance" to "funders of healthcare" may find themselves better positioned to control costs while still offering the high-value benefits necessary to win the talent war in an increasingly competitive market. The focus for the remainder of the decade will likely remain on cost containment, technological integration in wellness programs, and the continued adoption of personalized benefit structures.