As the fiscal year 2026 progresses, American business owners find themselves navigating a complex and increasingly expensive landscape regarding employee compensation and benefits. For the modern organization, health insurance has transcended its status as a standard "perk" to become the single most significant and volatile expense in the benefits portfolio. Driven by a confluence of rising hospital operational costs, a surge in the prevalence of chronic health conditions, and the skyrocketing demand for high-cost specialty medications, the financial burden of providing healthcare has reached a critical inflection point. Business leaders are no longer merely asking how to provide coverage, but are fundamentally questioning the long-term sustainability of traditional group health models as they scrutinize the actual cost per employee.

The urgency of this inquiry is underscored by the current labor market dynamics. Despite the high costs, abandoning health benefits is rarely a viable strategic option. Recent data from industry surveys, including those conducted by PeopleKeep, indicate that health coverage remains the most highly valued benefit among the American workforce, with a staggering 92% of employees ranking it as their top priority. In an era where talent retention and acquisition are paramount to operational success, the absence of a robust health benefit can lead to increased turnover and a diminished ability to compete for high-skilled labor. Consequently, understanding the average expenditures for group health insurance and exploring emerging alternative models has become a mandatory exercise for budget-conscious executives.

The Financial Reality of Group Health Insurance in 2026

Traditional group health insurance remains the dominant vehicle for employer-sponsored coverage, yet its cost structure continues to challenge corporate balance sheets. In 2026, the market primarily utilizes two frameworks: fully-insured plans and self-funded plans. In a fully-insured model, the employer pays a fixed premium to an insurance carrier, which then assumes the financial risk of medical claims. While this offers budget predictability, it often comes with rigid "one-size-fits-all" structures and minimum participation requirements that may not align with a diverse workforce’s needs.

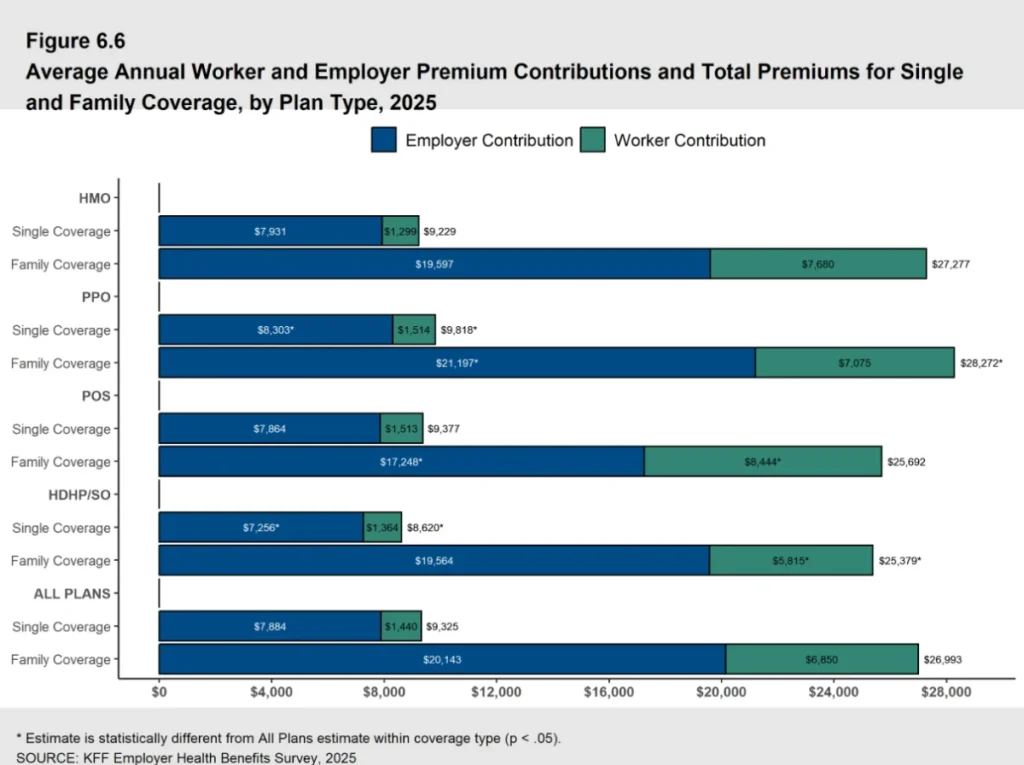

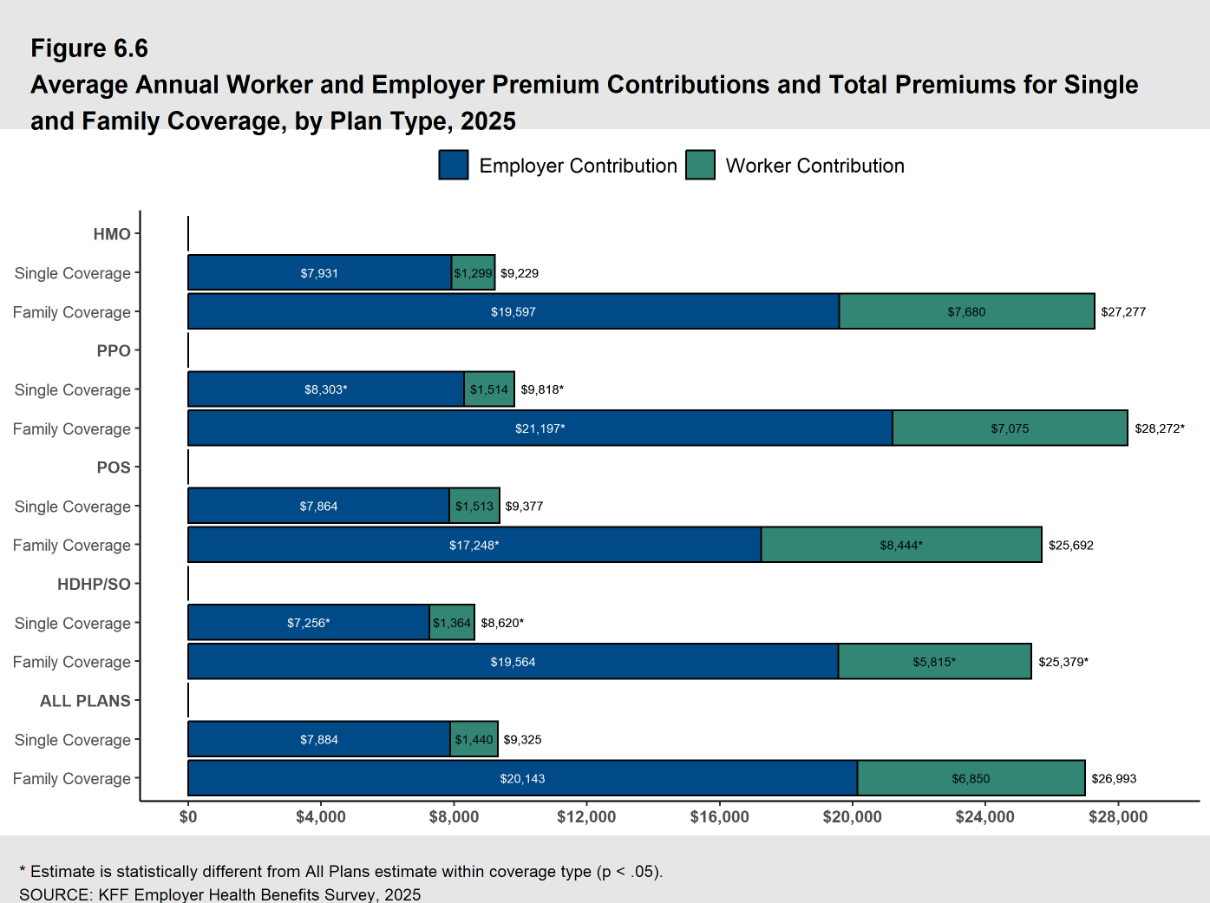

According to the KFF 2025 Employer Health Benefits Survey, which serves as a foundational benchmark for current 2026 projections, the average annual cost of employer-sponsored health insurance premiums has reached unprecedented levels. For family coverage, the average annual premium stands at $26,993, while single coverage has risen to $9,325. These figures represent a significant escalation from the previous decade, fueled by an annual trend of increasing premiums that shows no signs of abating.

For organizations that choose the self-funded route, the financial mechanics differ but the underlying cost pressure remains. In this model, the employer pays for medical claims directly as they are incurred, often utilizing a third-party administrator (TPA) and purchasing "stop-loss" insurance to mitigate the risk of catastrophic claims. While self-funding can offer greater transparency and potential savings during "healthy" years, it exposes the organization to direct volatility in healthcare utilization.

A Decade of Escalation: The Chronology of Rising Premiums

To understand the current crisis, one must look at the historical trajectory of healthcare costs. The average premium for family coverage has experienced a 26% increase over the last five years and a nearly 47% increase over the last decade. This steady climb is not merely a reflection of general inflation but is tied to specific structural shifts in the healthcare industry.

- 2016–2020: Premiums saw moderate but consistent growth, largely driven by the rising costs of outpatient services and the introduction of new, expensive diagnostic technologies.

- 2021–2023: The post-pandemic era introduced labor shortages in the healthcare sector, leading to higher hospital operating costs which were eventually passed down to insurers and employers.

- 2024–2026: The current period is defined by the "Specialty Drug Surge." The widespread adoption of GLP-1 agonists for weight loss and diabetes, along with the arrival of several multi-million-dollar gene therapies, has placed a new level of strain on pharmacy benefit portions of health plans.

PwC’s Health Research Institute recently reported that healthcare cost increases have stabilized at a high plateau, with an 8.5% projected increase for group insurance plans in 2026. This represents a 3% jump in the growth rate since 2022, signaling that the "inflationary floor" for healthcare has moved upward.

Breaking Down the Contributions: Who Pays What?

The total premium is only one part of the story; the distribution of that cost between the employer and the employee determines the plan’s perceived value and the business’s actual liability. In 2025 and 2026, the average employer contribution has remained relatively stable in terms of percentage, even as the dollar amounts have climbed.

On average, employers are contributing 85% of the premium for single coverage and 75% for family coverage. In practical terms, this means an employer is paying approximately $7,884 annually for an individual employee and $20,143 for an employee with a family. For the employee, the remaining balance—$1,440 for single and $6,850 for family coverage—is typically deducted from their gross pay on a pre-tax basis.

While the percentage split appears generous, the absolute dollar amount required from employees is becoming a point of friction. As the employee’s share of family coverage approaches $7,000 annually, many workers find themselves "underinsured" or struggling with the affordability of their own employer-provided benefits, particularly when deductibles and co-pays are factored into the equation.

Strategic Cost Control and the Shift to HRAs

Faced with these escalating figures, a growing number of organizations are moving away from traditional group plans in favor of "defined contribution" models, specifically Health Reimbursement Arrangements (HRAs). This shift represents a fundamental change in philosophy: rather than choosing a specific plan for the employee (defined benefit), the employer provides a set dollar amount that the employee can use to purchase their own coverage (defined contribution).

The Individual Coverage HRA (ICHRA)

The ICHRA has emerged as a powerful tool for businesses of all sizes. It allows employers to reimburse employees tax-free for individual health insurance premiums and other qualified medical expenses. This model provides the employer with total budget predictability—the company decides exactly how much it will contribute—while giving employees the freedom to choose a plan from the individual market that fits their specific doctor preferences and health needs.

The Qualified Small Employer HRA (QSEHRA)

For small businesses with fewer than 50 full-time equivalent employees, the QSEHRA offers a similar streamlined approach. Created by the 21st Century Cures Act, the QSEHRA allows small firms to provide a tax-free allowance for healthcare without the administrative complexity or high minimum participation requirements of a traditional group plan.

The Group Coverage HRA (GCHRA)

For organizations not yet ready to abandon their group plans, the GCHRA (or Integrated HRA) acts as a middle ground. Employers can switch to a lower-cost, high-deductible health plan (HDHP) to reduce premium expenses and then use a GCHRA to reimburse employees for the out-of-pocket costs that the higher deductible creates. This strategy effectively "insures the insurance," protecting employees from high deductibles while lowering the employer’s fixed premium costs.

Tax Implications and Regulatory Compliance

A critical component of the 2026 benefits strategy involves the tax treatment of these contributions. HRAs offer significant advantages: reimbursements are 100% tax-deductible for the employer and are excluded from the employee’s taxable income, provided the employee maintains "minimum essential coverage" (MEC).

In contrast, some employers have explored health insurance stipends—essentially adding extra funds to an employee’s paycheck for healthcare. However, stipends are considered taxable income, meaning both the employer and employee pay payroll taxes on those funds. Furthermore, for Applicable Large Employers (ALEs) with 50 or more employees, stipends do not satisfy the Affordable Care Act’s (ACA) employer mandate, potentially exposing the company to significant "shared responsibility" penalties.

The concept of "affordability" also plays a major role. Under the ACA, if an employer’s HRA offer is deemed "unaffordable" based on a percentage of the employee’s household income, the employee may choose to waive the HRA and instead access premium tax credits on the public exchange. This regulatory nuance requires careful calculation by HR departments to ensure compliance while maximizing the benefit’s value.

Broader Implications: The Future of the Employer-Employee Compact

The current state of health insurance costs is forcing a re-evaluation of the "employer-employee compact." As healthcare consumes a larger share of the total rewards package, businesses are finding less room for salary increases and other benefits. This has led to a rise in "ancillary" health strategies, such as telemedicine and wellness program incentives. By encouraging early identification of health issues and better management of chronic conditions, employers hope to bend the cost curve over the long term.

Industry analysts suggest that the trend toward personalization and portability in health benefits is irreversible. The "one-size-fits-all" group plan is increasingly viewed as an artifact of a previous economic era. In its place, the market is seeing a rise in "benefit marketplaces" where employees use employer-provided HRA funds to shop for customized coverage.

Conclusion

As we look toward 2027 and beyond, the data suggests that the "business as usual" approach to health insurance is no longer sustainable for many organizations. With average family premiums exceeding $26,000 and projected annual increases of 8.5%, the financial pressure is immense. However, the emergence of HRAs and the evolution of the individual insurance market provide a path forward. By transitioning to defined contribution models, employers can regain control over their budgets while still providing the high-value health benefits that are essential for maintaining a dedicated and healthy workforce. The challenge for 2026 and beyond will be for leaders to balance these financial realities with the human need for accessible, affordable, and high-quality medical care.