Despite a persistent backdrop of volatile pressures that continue to temper immediate business forecasts, year-ahead manufacturing confidence has experienced a moderate improvement this month, signaling a cautious optimism among industry leaders. This uptick, detailed in the latest Chief Executive CEO Confidence Index Survey, suggests a growing conviction that current global economic headwinds, while significant, may begin to recede in the coming twelve months.

Navigating a Multi-Pronged Threat Landscape

The manufacturing sector has been grappling with a complex web of challenges since late 2025. The confluence of ongoing international conflicts, marked by geopolitical instability and disruptions to global trade routes, has been a primary concern. This instability directly feeds into price volatility across a spectrum of essential raw materials and components, making long-term financial planning exceedingly difficult. Compounding these issues are the specter of regulatory changes, which can introduce unforeseen compliance costs and operational adjustments, and the persistent threat of inflationary conditions, which erode purchasing power and increase the cost of doing business.

These interconnected stressors have created a multi-pronged threat for manufacturing leaders, casting a long shadow over their current business sentiment. However, the latest survey data reveals a discernible shift, with a majority of U.S. manufacturers expressing a firm belief that a resolution to these challenges is on the horizon within the next year. This forward-looking perspective is crucial for maintaining investment and operational momentum in a turbulent environment.

Current Conditions Hold Steady, Future Outlook Brightens

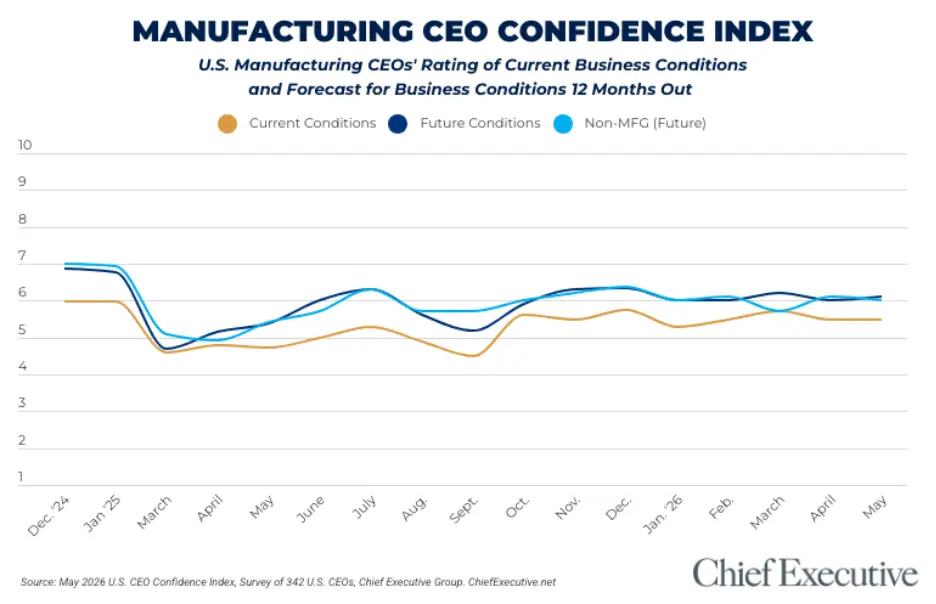

The Chief Executive CEO Confidence Index Survey, conducted from May 5-6, polled 342 U.S. CEOs. The findings indicate that manufacturers are maintaining a steady, albeit cautious, stance regarding current business conditions. They rated these conditions at an average of 5.5 out of 10, where 1 signifies poor performance and 10 represents excellent conditions. This rating has remained relatively stable, hovering around the 5.5 mark since February 2026. This period coincides with the intensification of the conflict in the Middle East, which significantly amplified supply chain concerns for manufacturing leaders. While this level reflects a challenging environment, it is notably an improvement compared to the sentiment experienced throughout much of the previous year.

The more encouraging news lies in the projections for the next twelve months. When asked about their expectations for the coming year, manufacturers anticipate a tangible improvement in business conditions. They forecast the Index to rise to 6.0 out of 10 by this time next year. This represents a 2 percent increase since April and signifies a notable turn towards optimism. A significant 52 percent of U.S. manufacturers share this positive outlook. This recovery in optimism is particularly welcome, as it begins to counteract the 3 percent decline in the Index that was recorded last month, underscoring the sector’s resilience and adaptive capacity.

A Divergent Path from Broader CEO Sentiment

Interestingly, manufacturers are currently charting a different course than the broader CEO population surveyed in May. While overall ratings of current conditions for manufacturers have seen a slight improvement, the outlook for future forecasts among the general CEO pool has declined by 1 percent since April. This divergence suggests that manufacturing leaders, despite facing similar macro-economic pressures, are exhibiting a distinct level of confidence in their sector’s near-term prospects. This contrasts with a growing number of CEOs across other sectors who appear to be adopting a more cautious "wait and see" approach, potentially delaying investment decisions and strategic planning until greater clarity emerges.

Drivers of Optimism: Demand, Resolution, and Innovation

Several factors are contributing to this optimistic shift within the manufacturing sector. A key driver appears to be improved demand, particularly in specific sub-sectors such as technology and consumer products. These areas, often more agile and responsive to market shifts, are showing signs of robust recovery and growth. Furthermore, there is a growing belief among manufacturers that the current period of volatility will begin to abate before 2027, a sentiment that fuels forward-looking investment and strategic expansion.

Randy Colwell, CEO of Holloway America, a mid-sized industrial manufacturer, articulates this dual perspective. "Right now, our market is strong and material costs are steady," he stated, acknowledging the current positive trends. However, he also pointed to ongoing concerns: "higher interest rates and fuel costs may worsen the market." Despite these challenges, Colwell expressed hope for the future, particularly contingent on geopolitical developments. "Especially if the war in Iran slows, we see good growth in the next 12 months," he added, highlighting the interconnectedness of global events and economic forecasting.

Echoing this sentiment, Art Hamilton, president of Hamilton International, a mid-sized industrial fabrics manufacturer, offered a more direct prediction of favorable changes. "I believe the interest rates will be lower in the year ahead," Hamilton stated, anticipating a significant factor that could stimulate business. He also pointed to potential policy-driven growth: "also, the tariff refund will drive growth," suggesting that a favorable regulatory or trade development could provide a substantial boost to the sector.

Beyond these specific points, a broader aspiration among manufacturers is for a "slowdown in accelerating costs" and an increased focus on "growing market share through innovation." This desire for cost stabilization, coupled with a commitment to developing new products and processes, points towards a strategic approach to navigating the current economic climate and securing future competitive advantage.

Shifting Recessionary Forecasts and Non-Manufacturer Sentiment

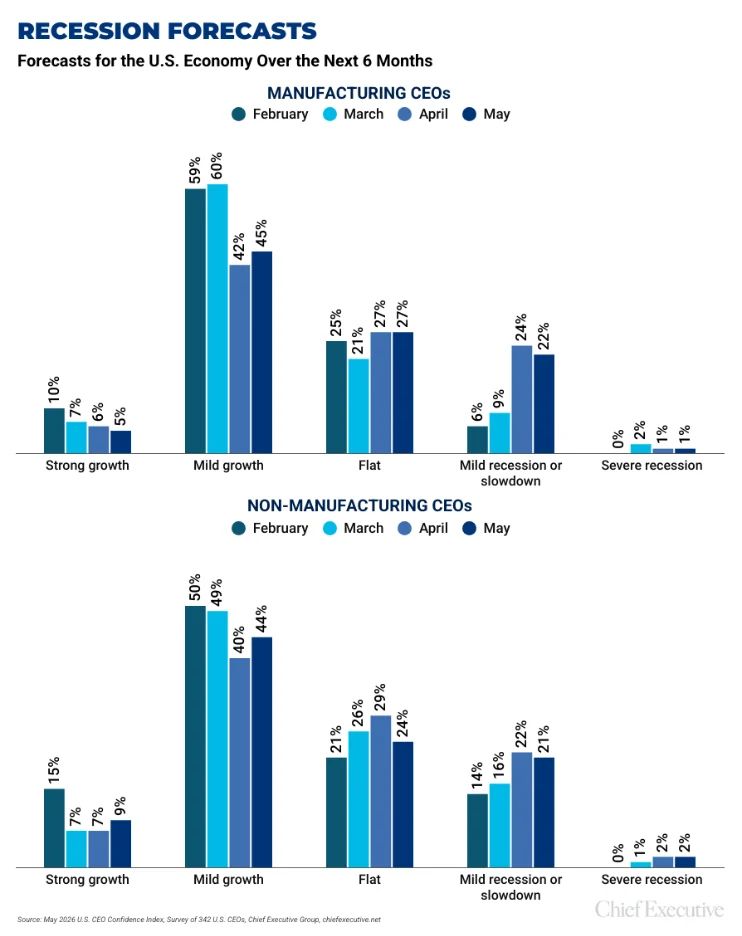

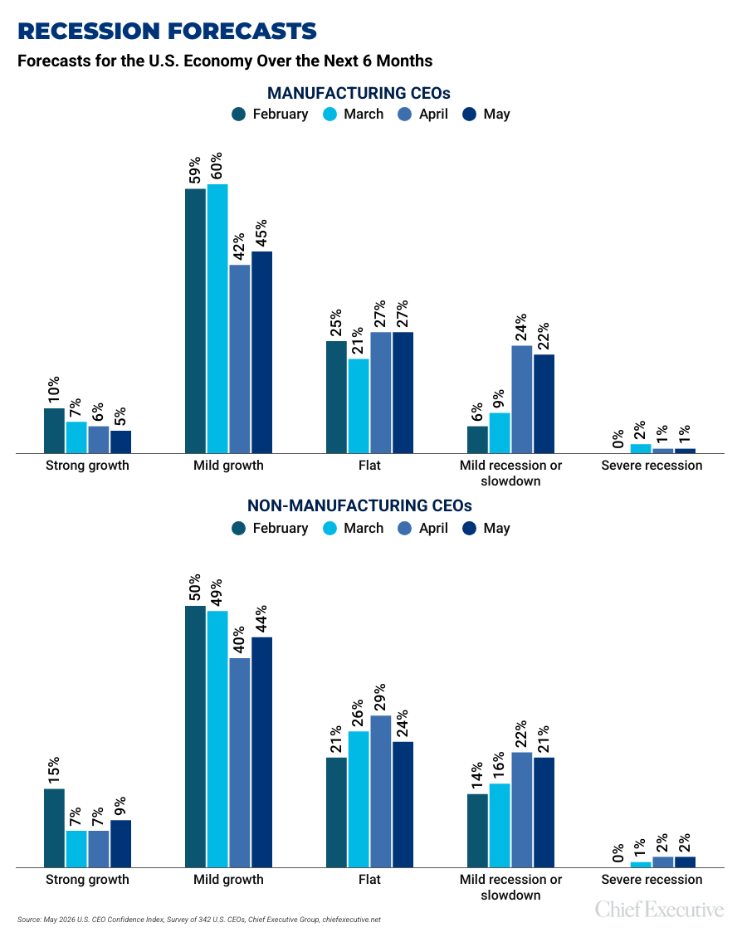

The increased optimism among manufacturers has also translated into a more favorable outlook regarding recessionary conditions. In May, recession forecasts saw an improvement, a welcome change after a significant worsening in April, which saw a substantial increase in the proportion of manufacturers expecting a recession. This month, exactly half of manufacturers project growth, a slight uptick from 48 percent in April. While a notable 23 percent still forecast recessionary conditions, this figure represents an improvement from April’s 25 percent, indicating a gradual de-escalation of recessionary fears.

In contrast, non-manufacturers, while generally more optimistic than their manufacturing counterparts in their forecasts, have taken a more pessimistic turn in their year-ahead outlook. Currently, 53 percent of non-manufacturers expect some form of growth in the next six months, an increase from 47 percent in April. This suggests that while non-manufacturing sectors might be projecting growth, the overall confidence in the sustained trajectory of that growth might be wavering, leading to a more cautious approach to long-term planning.

The Ascendant Role of Artificial Intelligence

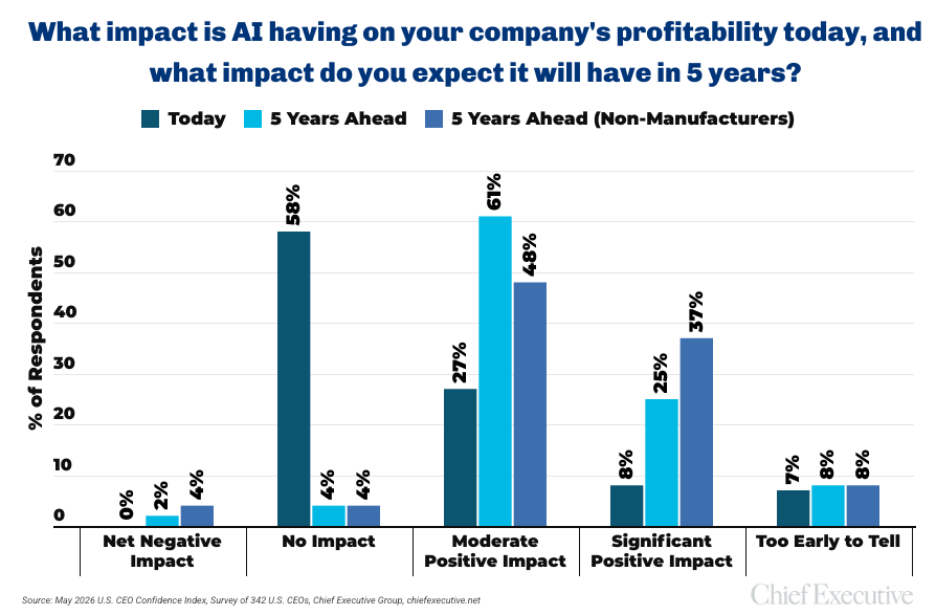

Amidst these evolving economic landscapes, artificial intelligence (AI) is emerging as a pivotal tool for manufacturing leaders navigating the current turbulent environment. The survey reveals a strong conviction among manufacturers regarding AI’s potential to significantly improve profitability by 2031.

Currently, however, the immediate impact of AI on company profitability is perceived as minimal by a majority of U.S. manufacturers. Fifty-eight percent of respondents reported that AI has no impact on their current profitability. This finding likely reflects the ongoing process of AI adoption within many organizations. Companies are still in the early stages of integrating AI technologies, defining their specific use cases, and establishing clear return on investment (ROI) metrics. The transformative potential of AI is, therefore, largely seen as a future development rather than an immediate operational reality.

When the time horizon shifts to the future, the perspective changes dramatically. A substantial 86 percent of manufacturing CEOs forecast that AI will have some form of positive impact on profitability within the next five years. The majority of these foresee a moderate impact, indicating a widespread expectation of AI’s gradual but significant contribution to bottom-line improvements.

Non-manufacturers, in comparison, tend to exhibit even greater enthusiasm for AI’s future capabilities. A notable 37 percent of non-manufacturers forecast a significant positive AI-driven impact on profitability five years down the line. This suggests a more aggressive expectation of AI’s disruptive and value-creating potential in sectors beyond traditional manufacturing.

Encouragingly, a very small minority within both groups anticipate net negative effects related to AI by 2031. Only 2 percent of manufacturers and 4 percent of non-manufacturers foresee negative consequences, underscoring the prevailing view that AI’s potential benefits far outweigh its risks.

Broader Implications and Future Outlook

The findings of the Chief Executive CEO Confidence Index Survey offer a nuanced perspective on the current state of the U.S. manufacturing sector. While immediate business conditions remain subject to significant global pressures, the upward trend in year-ahead manufacturing confidence is a positive indicator. This optimism is fueled by a combination of improving demand in key sub-sectors, a belief in the eventual resolution of geopolitical and economic volatilities, and a proactive embrace of innovation.

The divergence in outlook between manufacturers and the broader CEO community highlights the unique challenges and opportunities faced by the industrial sector. The manufacturing industry’s ability to adapt and innovate, particularly in areas like AI integration, will be critical in navigating future economic cycles and maintaining its competitive edge on the global stage. As the sector moves towards a projected improvement in conditions, continued monitoring of key economic indicators, geopolitical developments, and technological advancements will be essential for sustained growth and stability.

About the CEO Confidence Index

Since 2002, Chief Executive Group has been diligently polling hundreds of U.S. CEOs across organizations of all types and sizes to compile its comprehensive CEO Confidence Index data. This Index serves as a vital barometer, tracking CEO confidence in both current and future business environments. It is meticulously constructed based on CEOs’ observations of a wide array of economic and business components, providing invaluable insights into the prevailing sentiment within the corporate landscape. For additional information regarding the Index and data from previous months, interested parties are encouraged to visit ChiefExecutive.net/category/CEO-Confidence-Index/.