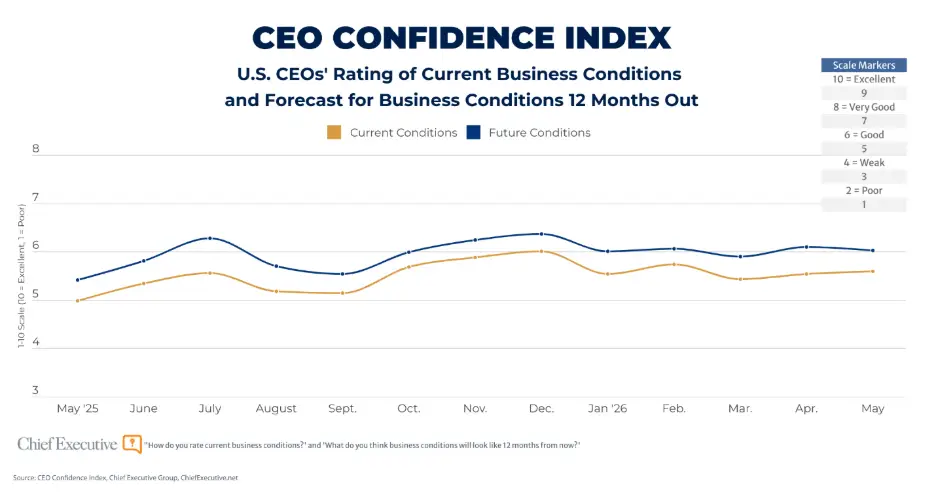

The landscape of American business sentiment has shifted, with a discernible cooling in optimism among Chief Executive Officers regarding the next 12 months. While current business conditions remain relatively stable, a notable decrease in the percentage of CEOs anticipating improvement signals a collective move toward a more cautious "wait and see" stance. This recalibration of outlook is largely attributed to a confluence of persistent geopolitical uncertainties, escalating costs, and ongoing policy ambiguity, according to the latest findings from Chief Executive’s May CEO Confidence Index.

The survey, which polled nearly 350 U.S. CEOs between May 5th and 6th, revealed that only 48 percent expect business conditions to improve over the coming year, a dip from 52 percent in April. This subtle but significant decline indicates a pause in forward momentum, rather than an outright downturn. The overall sentiment, however, has demonstrated remarkable resilience, with the index for current business conditions showing minimal fluctuation. CEOs rated the present economic climate at 5.6 out of 10, a marginal increase from April’s 5.5 and holding steady as the second-highest reading of 2026 thus far, trailing only February’s 5.7.

Similarly, the forward-looking component of the index, which gauges CEOs’ 12-month outlook, remained relatively stable at 6.0 out of 10, a slight decrease from April’s 6.1. This figure represents an anticipated improvement of approximately 8 percent by this time next year. Notably, this forward-looking metric has hovered around this level since the beginning of the year, suggesting a consistent, albeit tempered, expectation of growth.

The Dual Nature of Global Events: Drivers of Both Optimism and Pessimism

The key drivers influencing CEO sentiment – geopolitics, costs, demand, and policy – have remained consistent in recent months. However, the May data highlights a fascinating divergence in how these factors are being interpreted. Geopolitical events, in particular, are proving to be a double-edged sword. While 57 percent of CEOs who anticipate worsening conditions cited geopolitical issues as a primary concern, a substantial 43 percent of those expecting improvement also pointed to these same global dynamics.

For those leaning towards pessimism, concerns often revolve around the cascading effects of tariffs, persistent supply-chain disruptions, soaring energy costs, and a perceived weakening in consumer demand. Conversely, for the optimists, geopolitical developments are seen as potential catalysts for relief. One CEO succinctly captured this hopeful perspective, stating, "Iran conflict resolution within 3 months reducing oil prices and continued consumer confidence." Another echoed this sentiment, anticipating, "Geopolitics calming down, return of consumer confidence." This duality underscores the complex and multifaceted impact of international relations on the corporate psyche, where potential resolutions can foster optimism just as readily as ongoing conflicts breed apprehension.

The outlook on inflation exhibits a similar dichotomy. A significant 46 percent of pessimistic CEOs identified costs or inflation as key factors shaping their forecasts. Yet, intriguingly, 38 percent of optimistic CEOs also acknowledged inflation’s influence, albeit with a different perspective. For some, rising costs are directly impacting demand. As one CEO articulated, "Uncertainty of future costs is influencing demand." Others, however, foresee a reversal, with one CEO writing, "Gas prices will come down, which will lead to overall costs coming down." This indicates a segment of business leaders who believe inflationary pressures are temporary and will subside, thereby paving the way for improved cost structures.

Demand as a Lingering Beacon of Hope Amidst Uncertainty

Demand, however, continues to serve as a significant positive driver for many CEOs’ outlooks. A robust 38 percent of optimistic CEOs cited factors such as demand, customer engagement, market activity, order pipelines, backlogs, or growth opportunities as the basis for their upbeat projections. The CEO of a large construction firm, for instance, offered a particularly strong forecast for business conditions a year out, rating it an 8 out of 10 – a figure considerably above the survey average. This optimism was directly linked to "strong new project orders, growing backlog and increasing opportunities."

Further illustrating this point, another CEO reported, "Increased quote activity, booked results YTD up over last year, so far able to recover cost increases." Adding to this positive sentiment, a third executive noted, "More PO’s are starting to come in and more RFQ’s are coming in as well. The market is just cautious now." This suggests that while the broader economic climate may be fostering a degree of caution, underlying demand signals remain robust for many businesses, providing a foundation for continued activity and potential growth.

A Shift Towards Neutrality: The Rise of the "Flat" Outlook

While fewer CEOs are actively predicting a robust year ahead, there is also no sharp descent into widespread negativity. The percentage of CEOs expecting conditions to worsen remained relatively stable at 23 percent, a figure largely unchanged from the previous month. The real shift, therefore, has occurred in the middle ground. Thirty percent of CEOs now anticipate business conditions to remain flat over the next 12 months, an increase from 26 percent in April. This growing cohort reflects a prevailing sentiment of cautious pragmatism, where businesses are neither anticipating significant gains nor anticipating substantial losses.

This observed trend aligns with the qualitative feedback provided by CEOs throughout the survey. Many describe a business environment characterized by continuous activity but hampered by limited visibility, making precise forecasting a significant challenge. The prevailing atmosphere is one of navigating a steady stream of events that make long-term strategic decision-making difficult. As the CEO of a mid-sized professional services firm aptly put it, "A non-stop stream of events standing in the way of leaders making long term decisions."

Even businesses with strong current indicators are tempering their long-term outlooks due to broader uncertainties. A CEO from an upper-middle-market firm, despite reporting a "strong backlog presently, and opportunities are still strong," acknowledged, "Uncertainty in the world creates a less optimistic look for the next year." This sentiment highlights the pervasive influence of the external environment on internal strategic planning, even when current operational metrics are positive.

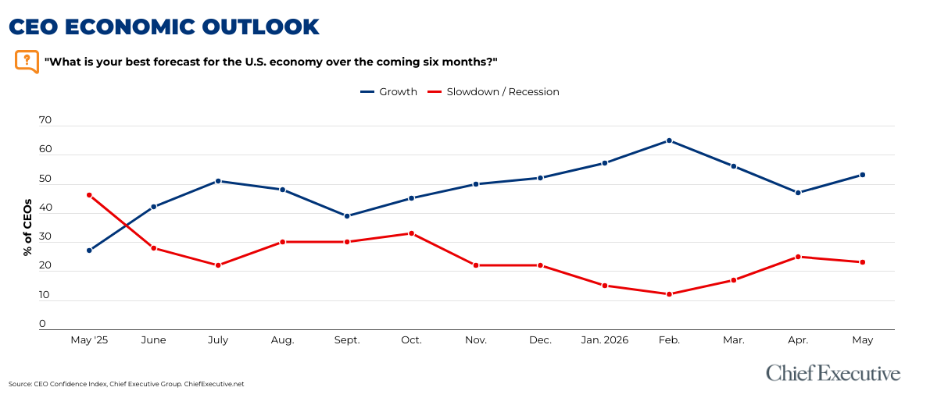

Economic Projections: Easing Recession Fears, Lingering Inflation Concerns

Shifting focus to broader economic forecasts, recessionary expectations saw a slight easing in May, following a spike in April that reached a six-month high. A slim majority of CEOs, 53 percent, now anticipate economic growth in the coming months. However, this figure remains considerably below the recent peak of 65 percent observed in February, before the onset of heightened geopolitical tensions.

Inflation expectations also showed signs of moderation. The average forecast for the 12-month Headline Consumer Price Index (CPI) rate dropped to 3.6 percent in May, down from 4.6 percent in April. This brings the average expectation back in line with the 3.5 percent readings recorded in the months prior to April’s surge.

However, a more nuanced picture emerges when examining the median inflation forecast. While the average declined, the median prediction for inflation continued its gradual upward trend. It rose from 3.0 percent in February and March to 3.3 percent in April, and further to 3.5 percent in May. This indicates that while the extreme end of inflation expectations may have softened, a significant portion of CEOs still anticipate inflation settling at a somewhat higher level than they projected earlier in the year. This suggests a persistent undercurrent of price pressure that may continue to influence business planning and consumer behavior.

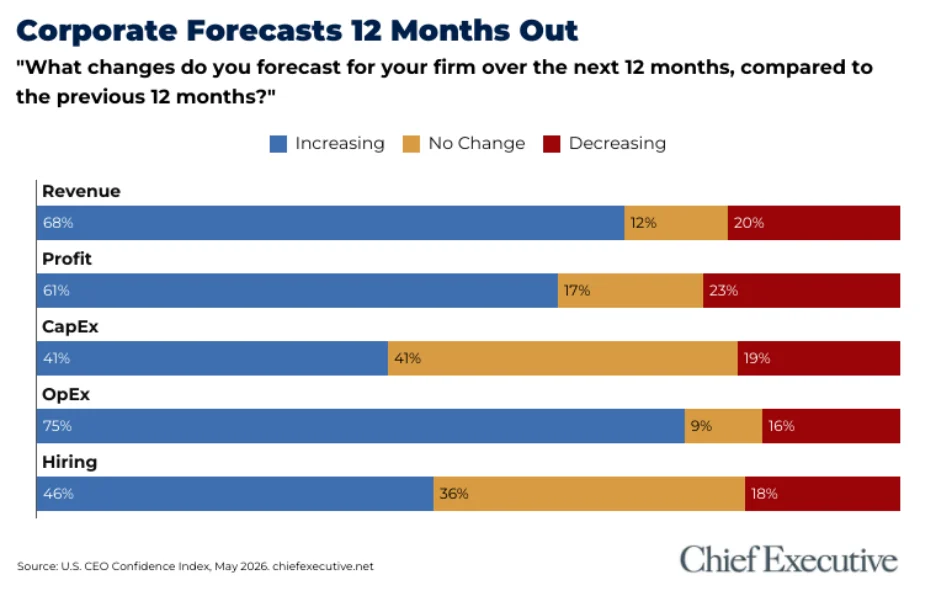

Corporate Forecasts: Cautious Hiring Amidst Rising Operating Expenses

The prevailing caution is also reflected in CEOs’ forecasts for their own companies. While specific details on corporate revenue, profit, and investment forecasts were not fully elaborated in the provided text, the overarching trend suggests a tempering of ambitious growth targets.

Hiring, however, emerges as a notable exception to this general trend of caution. In May, 46 percent of CEOs indicated plans to increase headcount, a slight uptick from 44 percent in April. Despite this modest rise, the figure remains significantly below the expectations at the start of the year, when 53 percent of CEOs anticipated expanding their workforce. This suggests that while companies are cautiously optimistic about hiring, the aggressive expansion seen earlier in the year has subsided.

A more consistent concern highlighted in the survey pertains to operating expenses. An overwhelming 75 percent of CEOs expect their operating costs to increase over the next 12 months, a finding that underscores the persistent inflationary pressures impacting businesses across sectors. This elevated expectation for rising expenses will likely continue to shape pricing strategies, cost-management initiatives, and profitability projections for the foreseeable future.

Background and Context: A Volatile Global Environment

The period leading up to May 2026 has been marked by significant global turbulence. The "war in Iran," as mentioned in the text, refers to a hypothetical or ongoing geopolitical conflict that has demonstrably impacted global energy markets and broader economic stability. Such conflicts often lead to increased uncertainty regarding oil prices, which in turn affect transportation costs, manufacturing expenses, and consumer spending power. This heightened geopolitical risk is a primary driver behind the cautious sentiment observed among CEOs.

Furthermore, the economic landscape has been characterized by a complex interplay of post-pandemic recovery challenges, supply chain bottlenecks, and evolving monetary policies. Central banks worldwide have been grappling with how to manage inflation without stifling economic growth, leading to a period of policy uncertainty that resonates deeply with business leaders. The consistent mention of "policy" as a driver of sentiment points to the critical need for clear and predictable regulatory and fiscal frameworks to foster greater business confidence.

Broader Impact and Implications

The shift towards a "wait and see" approach among CEOs has several potential implications for the broader economy. A more cautious stance can lead to a deceleration in business investment, as companies defer major capital expenditures and strategic expansions until there is greater clarity on the economic outlook. This can, in turn, moderate job creation and slow overall economic growth.

The persistent expectation of rising operating expenses also poses a challenge. Businesses facing higher costs may be forced to absorb these increases, leading to reduced profit margins, or pass them on to consumers through higher prices, potentially exacerbating inflationary pressures. The delicate balance between managing costs and maintaining competitive pricing will be a critical factor for corporate success in the coming months.

However, the resilience of current business conditions and the underlying strength in demand for certain sectors offer a counterbalance to these concerns. The ability of some companies to recover cost increases and secure new orders suggests that sectors with robust demand fundamentals may continue to thrive despite broader economic headwinds.

Ultimately, the May CEO Confidence Index paints a picture of an American business landscape navigating a period of significant uncertainty. While current operations remain relatively stable, the outlook for the next 12 months is one of cautious pragmatism. The collective sentiment of waiting for clearer signals from the geopolitical and economic arenas will likely define strategic decision-making and investment patterns for the remainder of 2026. The coming months will be crucial in observing whether the anticipated resolution of geopolitical tensions and a stabilization of costs can indeed rekindle a more robust sense of optimism among U.S. business leaders.