As organizations navigate the mid-2020s, the landscape of employee compensation has been fundamentally reshaped by the escalating costs of medical care, making health insurance not merely a standard benefit but the most significant financial commitment an employer faces outside of direct wages. Driven by a complex confluence of rising hospital operational costs, a surge in chronic health conditions among the workforce, and an unprecedented demand for high-cost specialty medications, employer healthcare expenditures have maintained a steady upward trajectory for over a decade. By June 2026, the question for business owners has shifted from whether they should offer health insurance to how they can possibly sustain the rising premiums while remaining competitive in a tight labor market.

The State of Employer-Sponsored Coverage in 2026

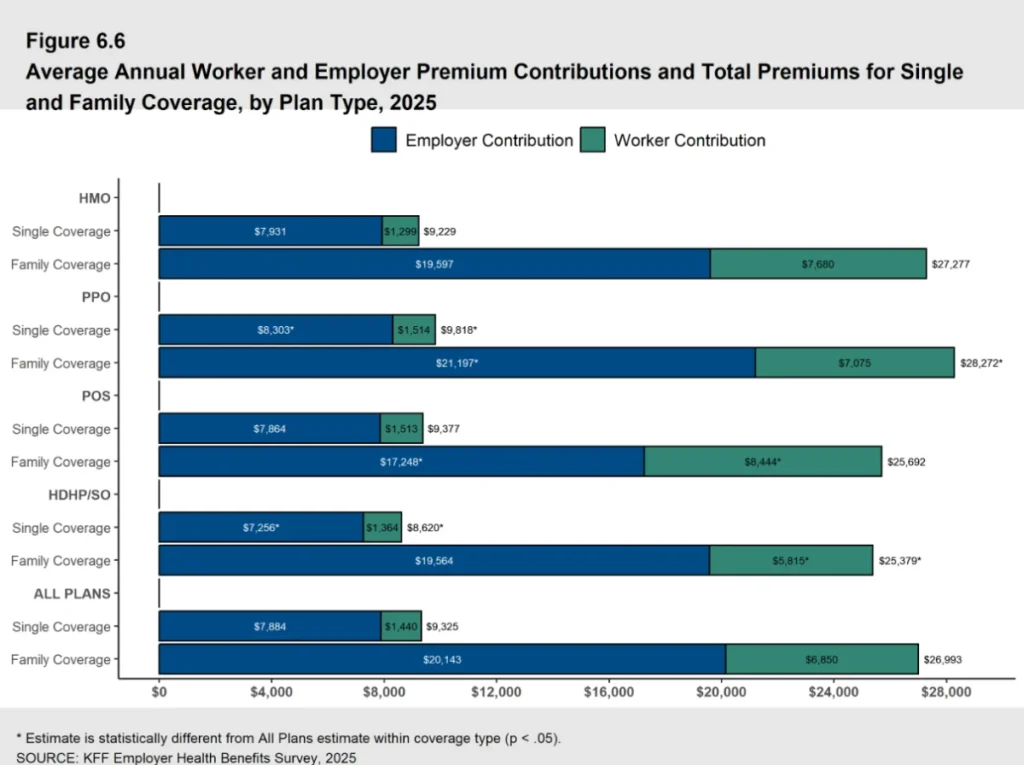

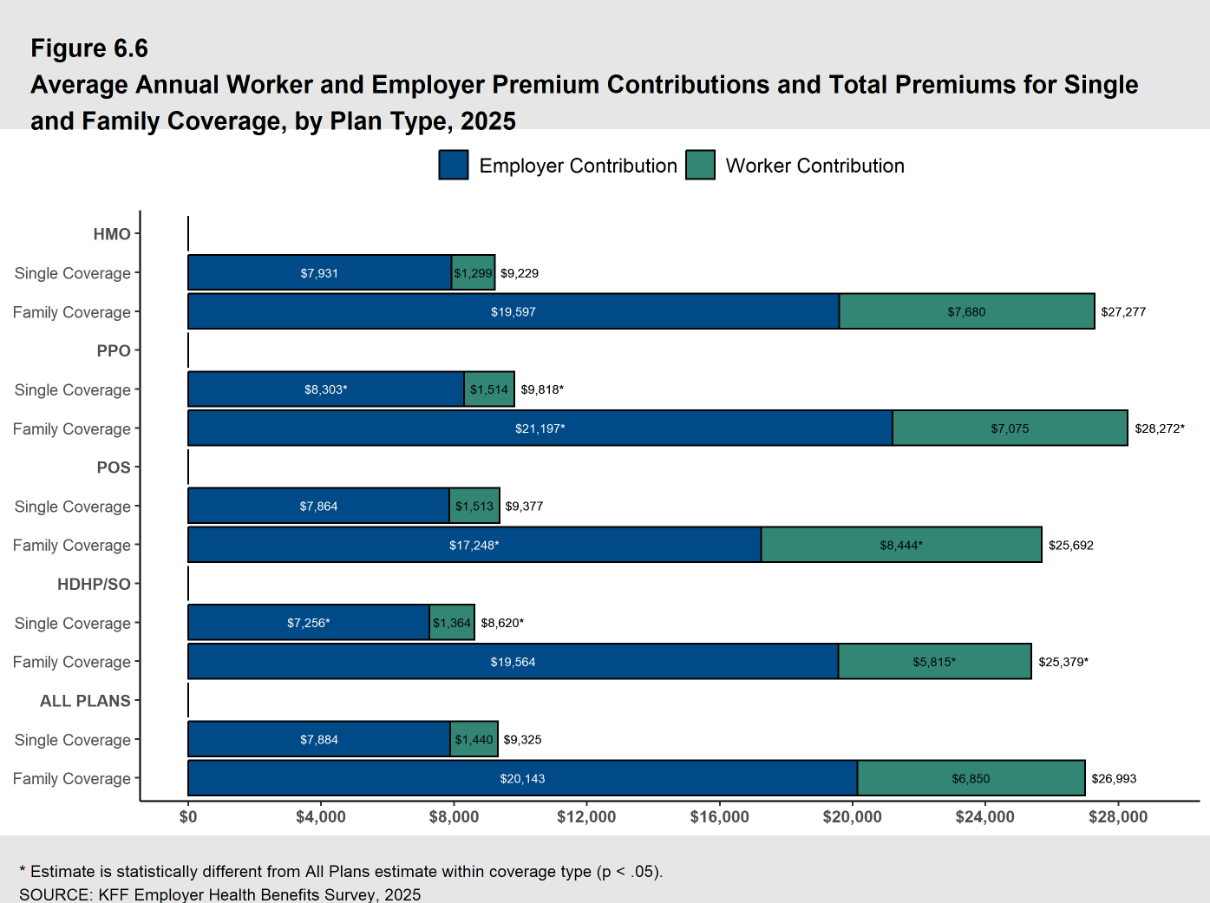

The financial burden of providing traditional group health insurance has reached a critical inflection point. According to the most recent data from the 2025 KFF Employer Health Benefits Survey, the average annual cost of employer-sponsored health insurance premiums reached $26,993 for family coverage and $9,325 for single coverage. These figures represent a significant jump from previous years, continuing a trend where family premiums have increased by 26% over the last five years and a staggering 47% over the last decade.

For the 2026 fiscal year, projections from PwC’s Health Research Institute indicate that healthcare cost growth shows no signs of slowing. Industry analysts report that average healthcare increases are holding steady at approximately 8.5% for group insurance plans. This persistent inflation is attributed to several "behind the numbers" factors, including the high cost of GLP-1 "blockbuster" drugs for weight loss and diabetes, the integration of expensive AI-driven diagnostic tools in clinical settings, and a general increase in the utilization of services as the aging workforce requires more intensive care.

A Chronology of Rising Costs: 2016–2026

To understand the current crisis, one must look at the decade-long evolution of the American healthcare economy. In 2016, the average family premium sat well below the $20,000 mark. However, several milestones accelerated the path to the current $27,000 average:

- 2016–2019: Moderate growth driven by standard inflation and the expansion of the Affordable Care Act (ACA) marketplaces.

- 2020–2022: The COVID-19 pandemic introduced extreme volatility. While utilization initially dropped during lockdowns, the subsequent return to care, combined with "long COVID" treatments and labor shortages in the nursing sector, drove costs upward.

- 2023–2025: Post-pandemic inflation hit the healthcare sector with a delay as multi-year contracts between insurers and hospital systems were renegotiated at significantly higher rates to account for increased labor and supply costs.

- 2026: The current year sees the full impact of specialty medication costs and the normalization of telehealth services, which, while convenient, have increased the overall volume of claims.

Analyzing the Employer-Employee Cost Split

The distribution of these costs remains a delicate balancing act for HR departments. In 2025, employers on average covered 75% of the premium for family plans and 85% for single plans. In dollar terms, this means an employer is contributing roughly $20,143 annually per employee for a family policy and $7,884 for a single policy.

From the employee’s perspective, the remaining portion—$6,850 for families and $1,440 for individuals—is typically deducted from gross pay on a pre-tax basis. While the employer bears the brunt of the premium, the employee’s "out-of-pocket" exposure through deductibles and co-pays has also expanded. This "hidden cost" often leads to employee dissatisfaction, even when the employer is paying a premium price for the coverage. Despite these costs, the "War for Talent" makes opting out of coverage a dangerous move; internal surveys from PeopleKeep indicate that 92% of employees still rank health insurance as their most valued benefit, making it the primary lever for employee retention.

Traditional Group Health Models: Fully-Insured vs. Self-Funded

Employers generally choose between two primary structures when providing group health insurance:

Fully-Insured Plans

In a fully-insured model, the employer pays a fixed premium to an insurance carrier. The carrier assumes the financial risk of medical claims. While this provides budget predictability, it often comes at a higher price point and includes "one-size-fits-all" restrictions that may not align with a diverse workforce’s specific needs. Furthermore, these plans are subject to strict minimum participation requirements, which can be difficult for small businesses with high turnover or part-time staff to meet.

Self-Funded Plans

Larger organizations often pivot toward self-funded plans, where the employer pays for medical claims directly as they occur. While this eliminates the "profit margin" of the insurance carrier, it exposes the business to the risk of catastrophic claims. To mitigate this, most self-funded employers purchase "stop-loss" insurance. This model offers more flexibility in plan design but requires sophisticated administrative oversight, often managed by a Third-Party Administrator (TPA).

Strategic Alternatives: The Rise of HRAs and Stipends

As traditional group plans become financially untenable for small to mid-sized enterprises (SMEs), many are turning to Health Reimbursement Arrangements (HRAs) as a way to control costs while still providing high-quality benefits.

The Individual Coverage HRA (ICHRA)

The ICHRA has emerged as a disruptive force in the benefits market. Unlike group plans, an ICHRA allows employers to set a monthly "defined contribution" (e.g., $500 per month). Employees then use that tax-free money to buy an individual health insurance plan on the open market that fits their specific doctor preferences and health needs. This shifts the risk of premium hikes away from the employer and onto the broader individual market, while giving the employer absolute budget predictability.

The Qualified Small Employer HRA (QSEHRA)

Designed specifically for businesses with fewer than 50 full-time equivalent employees, the QSEHRA allows small business owners to reimburse employees for premiums and qualified medical expenses. This is particularly effective for startups and small firms that cannot meet the participation or contribution requirements of traditional group plans.

Integrated Group Coverage HRAs (GCHRA)

For employers who wish to keep their group plan but need to lower their premiums, the GCHRA (or "Integrated HRA") is a common solution. The employer switches to a High Deductible Health Plan (HDHP) to lower the monthly premium and then uses an HRA to reimburse employees for the increased out-of-pocket costs, such as deductibles and co-pays.

The Role of Health Stipends and Tax Implications

For organizations that find HRAs too restrictive due to federal "affordability" mandates or complex compliance rules, health stipends offer a simpler, though less tax-efficient, alternative. A health stipend is essentially additional taxable wages earmarked for healthcare.

While flexible, stipends carry significant drawbacks:

- Taxation: Stipends are considered taxable income, meaning both the employer and employee pay payroll taxes on the funds.

- ACA Compliance: For Applicable Large Employers (ALEs)—those with 50 or more full-time employees—stipends do not satisfy the ACA’s employer mandate. Failure to offer "minimum essential coverage" can result in significant penalties.

- W-2 Reporting: Employers must meticulously track and report these payments as income, adding to the administrative load at year-end.

Implications for the Future of Work

The 2026 healthcare landscape suggests a fundamental shift in the social contract between employer and employee. We are moving from a "defined benefit" era, where the employer provided a specific insurance product, to a "defined contribution" era, where the employer provides a specific dollar amount for health expenses.

This shift has broad implications:

- Labor Mobility: Portability is becoming a key theme. HRAs like the ICHRA allow employees to keep their insurance plans even if they change jobs, provided the new employer also offers a reimbursement model.

- Small Business Competitiveness: By using HRAs, small businesses can finally compete with large corporations by offering "Gold" or "Platinum" level individual plans through reimbursement, which was previously cost-prohibitive.

- Provider Dynamics: As more employees move to the individual market via ICHRAs, insurance carriers are incentivized to improve their individual plan offerings, potentially stabilizing those markets.

Conclusion and Outlook

The trajectory of healthcare costs in 2026 serves as a wake-up call for the American business community. With group premiums for family coverage approaching $30,000, the traditional model is under immense pressure. While factors like hospital costs and specialty drugs continue to drive inflation, the emergence of HRAs and flexible reimbursement models provides a pressure valve for employers.

For the modern business owner, the goal is no longer just to "have insurance," but to manage a health benefit strategy that balances fiscal responsibility with the human need for security. As we look toward 2027 and beyond, the organizations that thrive will be those that move away from reactive premium-paying and toward proactive, defined-contribution strategies that empower employees to take control of their own healthcare journeys. Financial analysts and HR experts agree: the era of the one-size-fits-all group plan is fading, replaced by a more personalized, transparent, and budget-conscious approach to employee wellness.