The landscape of American healthcare in 2026 continues to be defined by a widening gap between the cost of medical services and the ability of the average citizen to afford them. As out-of-pocket expenses for prescriptions, specialist visits, and emergency care escalate, a significant portion of the population is being forced to make difficult choices regarding their physical well-being. According to data from KFF, 75% of uninsured adults in the United States reported skipping or postponing necessary medical care in 2025 due to prohibitive costs. Even among those with insurance, the financial strain remains palpable, with nearly half of all U.S. adults expressing difficulty in affording healthcare services. In response to this crisis, a growing number of employers are turning to Health Reimbursement Arrangements (HRAs) and health stipends to bridge the coverage gap, providing a tax-advantaged lifeline for employees struggling with the rising "hidden costs" of health insurance.

The Rising Ceiling of Out-of-Pocket Medical Expenses

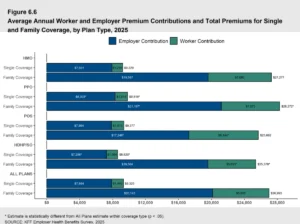

Out-of-pocket costs represent the portion of medical expenses that health insurance plans do not cover. These include deductibles, which must be met before insurance begins to pay; copayments, the fixed fees paid at the time of service; and coinsurance, the percentage of costs an individual pays after meeting their deductible. For many, the most daunting figure is the "out-of-pocket maximum," the absolute limit an individual or family is required to pay in a given year for covered, in-network services.

For the 2026 plan year, the Internal Revenue Service (IRS) has set these limits at $10,600 for individual policies and $21,200 for family policies. While these caps provide a safety net against total financial ruin in the event of a catastrophic illness, they remain significantly higher than the average American’s savings. Furthermore, these limits typically apply only to in-network care. When patients are forced to seek out-of-network services—often during emergencies or when specialists are unavailable—the financial exposure can become virtually unlimited.

The financial pressure is particularly acute for those managing chronic conditions. Ongoing requirements for specialized medication, regular diagnostic testing, and frequent consultations can quickly push a household toward their annual out-of-pocket maximum. Data indicates that approximately 30% of U.S. households struggled to pay a medical bill within the last 12 months, highlighting the inadequacy of traditional insurance premiums alone in providing comprehensive financial security.

A Chronology of Benefit Evolution: From Group Plans to Personalization

The shift toward employer-sponsored medical reimbursements has been decades in the making, accelerated by legislative changes and a transforming labor market. Historically, the "one-size-fits-all" group health insurance model was the standard. However, as premiums rose and employee needs became more diverse, the limitations of this model became apparent.

The introduction of the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) in late 2016 marked a pivotal shift, allowing small businesses to reimburse employees for individual insurance premiums and medical expenses tax-free. This was followed by the 2020 rollout of the Individual Coverage Health Reimbursement Arrangement (ICHRA), which expanded these benefits to companies of all sizes and allowed for greater customization based on employee classes.

By 2026, the adoption of these models has become a strategic necessity. With health coverage consistently ranking as the most-requested benefit in employee surveys, businesses are no longer viewing health benefits as a mere line item but as a critical tool for talent retention and recruitment. The chronology of this evolution reflects a broader trend toward the "personalization" of benefits, where employees are empowered to choose the care that best fits their specific health profile and budget.

Identifying Reimbursable Expenses Under IRS Guidelines

A central component of managing out-of-pocket costs is understanding which expenses are legally eligible for reimbursement. The IRS provides a comprehensive list under Publication 502, covering more than 200 types of medical, dental, and vision expenses. These items are categorized under Section 213(d) of the Internal Revenue Code.

Eligible expenses go far beyond the standard doctor’s office visit. They include:

- Preventative and Diagnostic Care: Routine physicals, lab tests, X-rays, and screenings.

- Prescription Medications: Insulin, specialized treatments, and birth control.

- Medical Equipment: Crutches, wheelchairs, hearing aids, and even home modifications for medical necessity.

- Vision and Dental: Eyeglasses, contact lenses, laser eye surgery, and non-cosmetic dental procedures.

- Mental Health Services: Therapy sessions, psychiatric care, and certain addiction treatment programs.

- Over-the-Counter (OTC) Items: Following legislative updates in recent years, many OTC medications and menstrual care products are now reimbursable without a prescription.

For employees, the ability to use pre-tax dollars—either through an HRA, a Health Savings Account (HSA), or a Flexible Spending Account (FSA)—to cover these costs represents a significant increase in purchasing power. For an employee in a 22% tax bracket, using an HRA to pay for a $1,000 medical procedure is the equivalent of receiving a $1,220 raise, as the funds are not subject to income or payroll taxes.

Strategic Implementation: HRA Models for the Modern Workplace

Employers looking to mitigate their staff’s financial burden have several sophisticated tools at their disposal. Each model offers different advantages depending on the size of the organization and the existing insurance infrastructure.

The Individual Coverage HRA (ICHRA)

The ICHRA has emerged as a powerhouse in the benefits world. It allows employers to provide a tax-free monthly allowance, which employees then use to purchase their own individual health insurance on the open market. Any remaining funds can be used to reimburse other out-of-pocket expenses. This model is particularly favored for its scalability and the way it removes the employer from the complexities of managing a group policy.

The Qualified Small Employer HRA (QSEHRA)

Designed specifically for businesses with fewer than 50 full-time equivalent employees, the QSEHRA is a streamlined option. It allows small business owners to support their team’s healthcare costs without the administrative overhead of a traditional plan. It is subject to annual contribution limits set by the IRS but offers maximum flexibility for the employee to choose their own provider.

The Group Coverage Integration HRA (GCHRA)

Also known as an integrated HRA, this model is designed for employers who wish to maintain a traditional group health insurance plan but want to supplement it. Often, an employer will choose a high-deductible health plan (HDHP) to keep premium costs low and then use the GCHRA to reimburse employees for the costs they incur before they hit their deductible. This "wrap-around" approach ensures that employees are not hit with high upfront costs.

The Alternative Approach: Health Stipends

While HRAs are highly regulated and offer the best tax advantages, some employers opt for health stipends. A stipend is a fixed sum of money added to an employee’s paycheck to help with healthcare costs.

The primary advantage of a stipend is its simplicity; there are no complex IRS reporting requirements or strict lists of eligible expenses. However, stipends come with significant drawbacks. They are considered taxable income, meaning both the employer and the employee must pay taxes on the funds. Furthermore, stipends do not satisfy the Affordable Care Act’s (ACA) employer mandate for organizations with 50 or more employees. Despite these limitations, stipends remain a popular choice for very small startups or for companies looking to provide "wellness" perks that fall outside the traditional medical scope, such as gym memberships or nutrition counseling.

Broader Economic Impact and Future Implications

The shift toward employer-funded reimbursements carries profound implications for the broader U.S. economy. By lowering the barrier to care, these programs can lead to a healthier, more productive workforce. When employees are not afraid of the cost of a doctor’s visit, they are more likely to seek preventative care, which can catch chronic illnesses early and reduce long-term healthcare spending.

From a labor market perspective, the "benefits war" is intensifying. As of 2026, the ability to offer a personalized health benefit is no longer just a perk for high-tech industries; it is becoming standard practice in retail, manufacturing, and hospitality. Analysis suggests that companies offering flexible health reimbursements see lower turnover rates and higher employee satisfaction scores.

However, the rise of HRAs also puts more responsibility on the individual. Employees must become "healthcare consumers," navigating insurance marketplaces and managing their own reimbursement claims. This has led to a secondary market of benefits administration software, such as PeopleKeep, which automates the compliance and documentation process, ensuring that both employers and employees remain within the bounds of IRS and ACA regulations.

Conclusion: The Path Forward for Healthcare Affordability

As the 2026 fiscal year progresses, the data remains clear: the cost of medical care is a primary source of anxiety for the American worker. The traditional model of employer-sponsored group insurance is no longer a universal solution in an era of skyrocketing out-of-pocket maximums and diverse medical needs.

By leveraging the tax advantages of HRAs, employers can provide a meaningful buffer against the financial shocks of the healthcare system. Whether through an ICHRA that empowers individual choice or an integrated HRA that supports a group plan, these arrangements represent a move toward a more sustainable and equitable benefits landscape. For the 75% of uninsured and the millions of underinsured Americans, the expansion of these reimbursement models is not just a matter of corporate policy—it is a critical necessity for financial and physical survival in a high-cost medical environment.