Despite ongoing geopolitical tensions and economic headwinds that continue to temper immediate business outlooks, U.S. manufacturers are demonstrating a renewed sense of optimism regarding the year ahead. This shift in sentiment, as revealed by the latest Chief Executive CEO Confidence Index Survey, indicates a growing conviction among industry leaders that resolutions to current challenges are on the horizon.

The manufacturing sector has been navigating a complex and volatile landscape since late 2025. A confluence of factors, including protracted international conflicts, significant price fluctuations across raw materials and energy, evolving regulatory frameworks, and the persistent specter of inflation, has created a multi-faceted threat environment. These stressors have cast a long shadow over the current business sentiment of manufacturing leaders. However, the May survey data suggests a notable pivot towards a more hopeful outlook for the next twelve months.

Current Conditions Hold Steady, Future Outlook Brightens

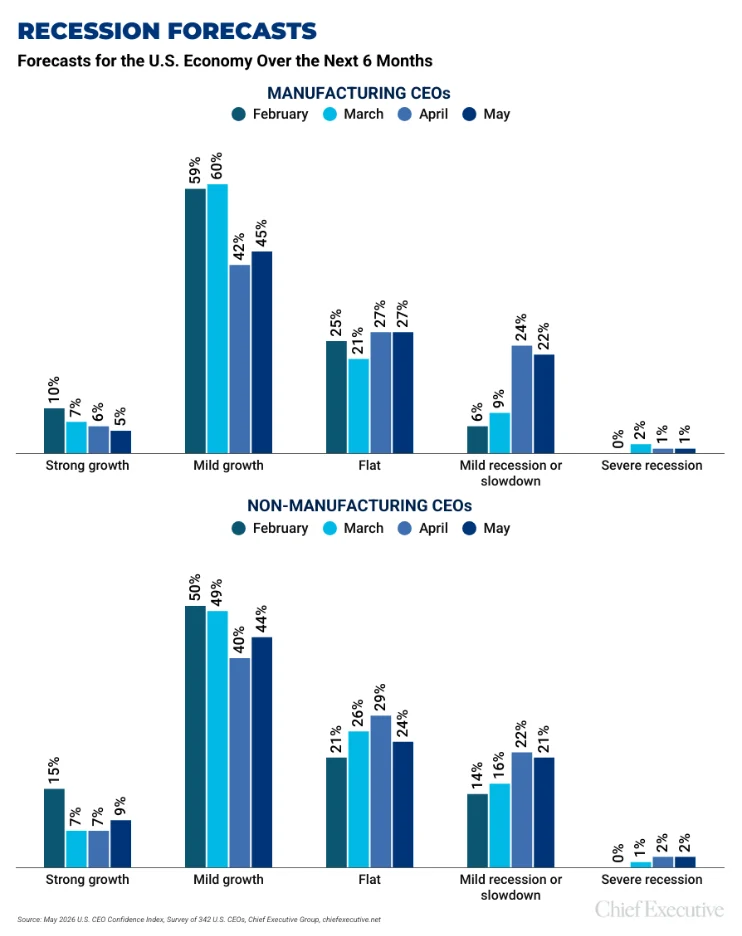

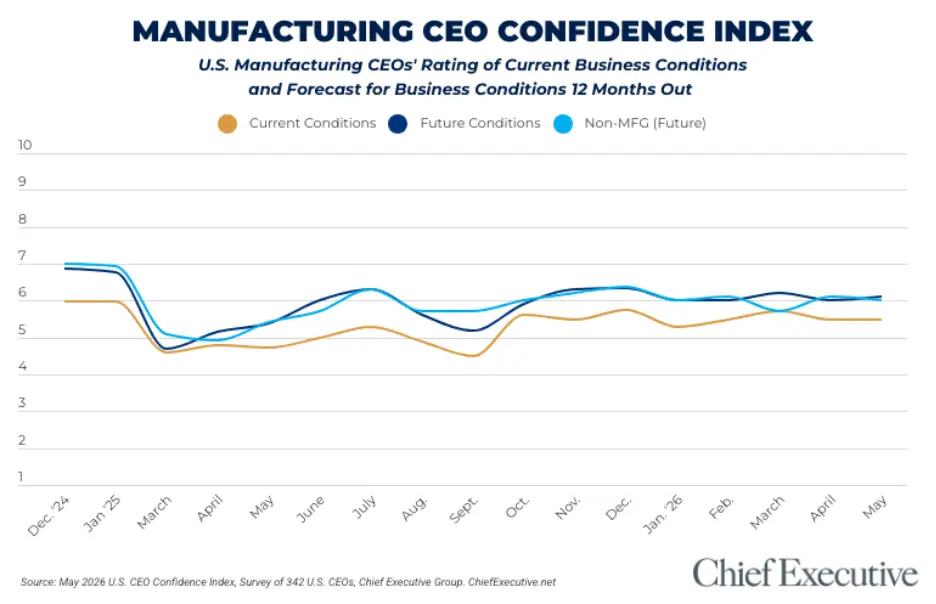

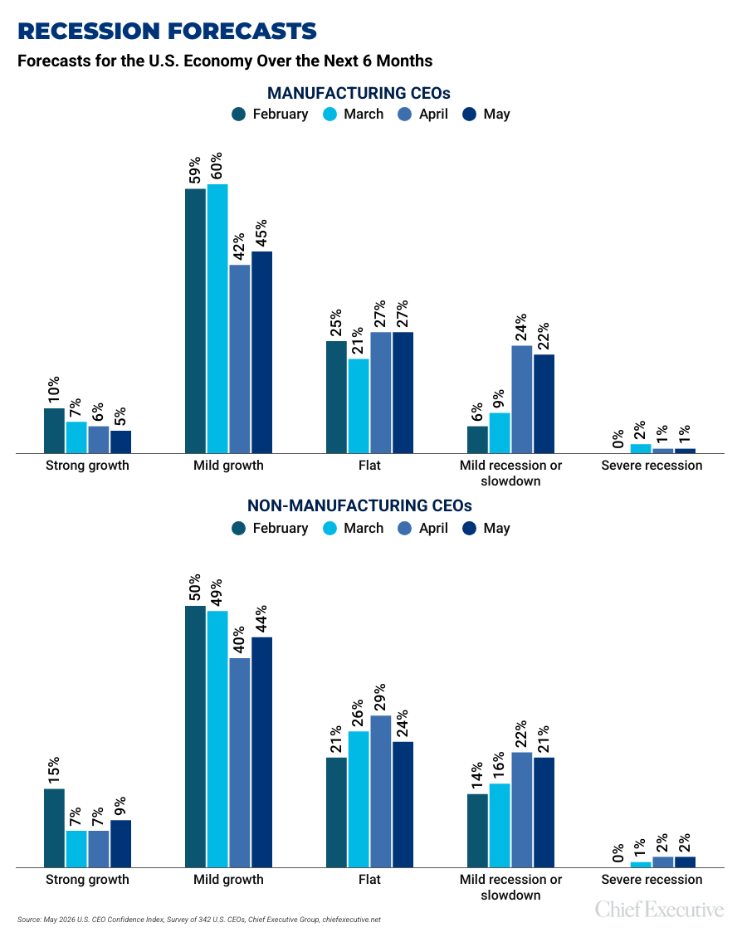

The Chief Executive CEO Confidence Index Survey, conducted from May 5-6 among 342 U.S. CEOs, found that manufacturers rated current business conditions at a 5.5 out of 10. This score, on a scale where 1 represents "Poor" and 10 signifies "Excellent," has remained remarkably consistent, hovering around the 5.5 mark since February 2026. This period coincides with the intensification of the conflict in the Middle East, which significantly impacted supply chain operations and became a primary concern for manufacturing executives. While current conditions have not dramatically improved, the stability is viewed positively, especially when contrasted with the more challenging sentiment prevalent for much of the preceding year.

The more compelling narrative emerges when examining year-ahead projections. Manufacturers anticipate a tangible improvement in business conditions over the next twelve months, forecasting an increase to 6.0 out of 10 by May 2027. This represents a 2 percent uptick from April’s projections, signaling a resurgence of optimism. A majority of U.S. manufacturers, precisely 52 percent, share this forward-looking positive outlook. This recovery is particularly significant as it partially mitigates the 3 percent decline in the index that was observed in the previous month, suggesting that recent headwinds may be perceived as temporary rather than indicative of a prolonged downturn.

A Divergent Path from Broader CEO Sentiment

Interestingly, manufacturers appear to be charting a different course than the broader CEO population polled in the same survey. While overall CEO ratings for current conditions saw a slight improvement, their future forecasts experienced a 1 percent decline in May. This suggests a growing number of CEOs across various sectors are adopting a more cautious "wait and see" approach, contrasting with the manufacturers’ growing conviction in an improved future. This divergence highlights the unique resilience and strategic outlook of the manufacturing industry in the face of broader economic uncertainties.

Drivers of Optimism: Demand Recovery and Resolution of Volatility

Several factors are contributing to this shift towards optimism within the manufacturing sector. A key driver is the perceived improvement in demand, particularly within the technology and consumer products sub-sectors. These areas, often sensitive to broader economic shifts, are showing signs of renewed strength, bolstering manufacturers’ confidence. Furthermore, there is a growing expectation among industry leaders that the current period of volatility, encompassing geopolitical and economic disruptions, will begin to resolve before the end of 2027.

Randy Colwell, CEO of Holloway America, a mid-sized industrial manufacturer, articulated this dual perspective. "Right now, our market is strong, and material costs are steady," he stated. "However, higher interest rates and fuel costs may worsen the market. Especially if the war in Iran slows, we see good growth in the next 12 months." His sentiment reflects the prevailing view that while immediate pressures persist, the potential for de-escalation in global conflicts and stabilization of input costs are critical determinants of future growth.

Art Hamilton, president of Hamilton International, a mid-sized industrial fabrics manufacturer, echoed this hopeful outlook. "I believe the interest rates will be lower in the year ahead," he commented. "Also, the tariff refund will drive growth." This perspective points to anticipated policy shifts and economic adjustments that could further catalyze the sector’s recovery.

Beyond these specific factors, a general desire for a "slowdown in accelerating costs" and an ambition to achieve "growing market share through innovation" are also shaping manufacturers’ optimistic outlook. This suggests a strategic focus on both cost management and competitive differentiation as key pathways to future success.

Shifting Recessionary Fears and Non-Manufacturer Outlook

The renewed optimism among manufacturers has also led to an improvement in recession forecasts for May. This comes after a significant deterioration in outlook in April, which saw a substantial increase in the proportion of manufacturers anticipating a recession. In the current survey, exactly half of manufacturers project economic growth, a slight increase from the 48 percent recorded in April. While the segment of manufacturers still forecasting recessionary conditions remains sizeable at 23 percent, this figure represents an improvement from April’s 25 percent, indicating a marginal but significant easing of recessionary fears.

In contrast, non-manufacturing sectors, while generally more optimistic than their manufacturing counterparts regarding immediate growth prospects, have shown a more pessimistic turn in their year-ahead forecasting. Currently, 53 percent of non-manufacturers expect some form of growth in the next six months, an increase from 47 percent in April. This suggests that while the broader economy might be seeing pockets of growth, the long-term outlook for non-manufacturing sectors is subject to a greater degree of uncertainty compared to the manufacturing industry.

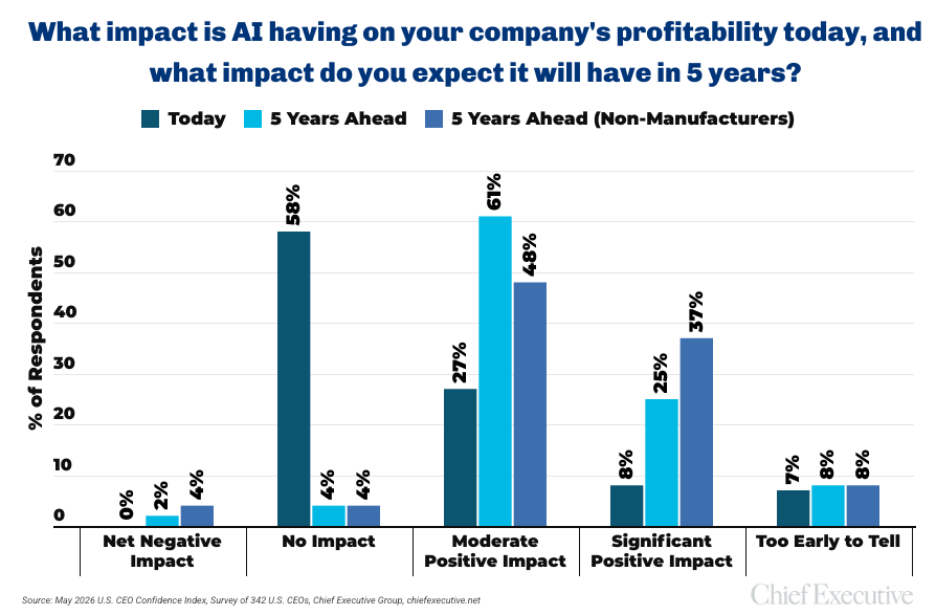

Artificial Intelligence: A Future Profitability Driver

Navigating the current turbulent environment necessitates the adoption of advanced tools, and artificial intelligence (AI) is increasingly recognized as a pivotal technology for manufacturers. While its impact on current profitability is still nascent, leaders are decidedly bullish on AI’s potential to significantly enhance earnings by 2031.

Currently, a majority of U.S. manufacturers, 58 percent, report that AI has no immediate impact on their company’s profitability. This finding is likely attributable to the ongoing process of AI adoption and integration within many organizations. Companies are still in the stages of onboarding new AI technologies and clearly defining their return on investment (ROI). The complexities of implementation and the learning curve associated with new technological paradigms mean that widespread, immediate profitability gains are not yet evident for most.

However, when the timeframe shifts to the future, the perspective changes dramatically. A substantial 86 percent of manufacturing CEOs forecast that AI will have a positive impact on profitability within the next five years. The majority of these anticipate this impact to be moderate, suggesting a steady and consistent improvement rather than an explosive surge. This long-term view indicates a strategic understanding of AI’s transformative potential.

Non-manufacturers, in comparison, tend to be even more bullish on AI’s future impact. A notable 37 percent of non-manufacturing CEOs forecast a significant positive AI-driven impact on profitability five years down the line. This suggests a higher degree of confidence in AI’s capacity to drive substantial, game-changing improvements in their respective industries.

Encouragingly, the forecast for negative AI impacts remains a slim minority for both groups. Only 2 percent of manufacturers and 4 percent of non-manufacturers anticipate net negative effects related to AI by 2031. This near-universal positive outlook on AI’s future potential underscores its perceived importance as a driver of innovation and economic growth in the coming years.

The CEO Confidence Index: A Barometer of Industry Sentiment

The Chief Executive CEO Confidence Index has been a crucial tool for tracking the pulse of American business leaders since its inception in 2002. This ongoing survey, conducted by Chief Executive Group, polls hundreds of U.S. CEOs from organizations of all types and sizes. The Index meticulously tracks confidence levels in both current and future business environments by gathering insights on various economic and business components. The consistent methodology and broad participation provide a reliable barometer of industry sentiment, offering valuable perspectives on the challenges and opportunities facing the U.S. economy. For further information on the Index and historical data, readers are encouraged to visit ChiefExecutive.net/category/CEO-Confidence-Index/.