As the global labor market continues to undergo a profound transformation, the traditional definition of employee compensation is being fundamentally rewritten. While salary remains a primary driver for job seekers, the peripheral components of a compensation package—known as ancillary benefits—have moved from the sidelines to the center of corporate strategy. These supplemental offerings, which range from dental and vision insurance to mental health support and pet insurance, are no longer viewed as mere "perks" but as essential tools for recruitment, retention, and workforce stability. In an era where 81% of employees report that a comprehensive benefits package is a deciding factor in whether they accept a job offer, businesses of all sizes are re-evaluating how they fill the gaps left by major medical coverage.

Understanding the Framework of Ancillary Benefits

Ancillary benefits are secondary insurance products and non-medical perks offered alongside a primary group health insurance plan. These benefits are generally categorized into two types: employer-funded and voluntary. In employer-funded models, the company pays a portion or the entirety of the premium, whereas voluntary benefits allow employees to access discounted group rates for coverage they pay for themselves via payroll deductions.

The scope of these benefits has expanded significantly over the last decade. Historically, ancillary coverage was limited to dental and vision plans. However, the modern definition has broadened to include life insurance, disability insurance, critical illness coverage, and lifestyle-focused stipends. These offerings serve a dual purpose: they provide financial security for employees facing unexpected life events and allow employers to tailor their benefits to a multi-generational workforce with diverse needs.

The Chronological Shift: From Standardization to Personalization

The history of employer-sponsored benefits in the United States dates back to the mid-20th century, but the move toward ancillary diversification is a more recent phenomenon.

- The Post-WWII Era (1940s–1950s): Following the 1942 Stabilization Act, which froze wages to prevent inflation, employers began offering health insurance as a way to compete for labor without violating federal law. This established the "one-size-fits-all" group health model.

- The Rise of Specialty Insurance (1970s–1990s): Dental and vision insurance became standardized additions to the corporate package as medical costs began to climb and specialized care became a distinct financial burden for families.

- The Affordable Care Act Era (2010–2019): With the implementation of the ACA, the focus shifted toward "Essential Health Benefits." However, as deductibles for major medical plans rose, employees began seeking "gap fillers"—supplemental policies like critical illness and hospital indemnity insurance to cover out-of-pocket costs.

- The Pandemic and Remote Work Pivot (2020–Present): The COVID-19 pandemic accelerated the demand for non-traditional benefits. Remote work highlighted the need for home office stipends, mental health resources, and flexible wellness programs. This era marked the transition from "standard" benefits to "personalized" benefits, where employees expect choices that reflect their specific lifestyles.

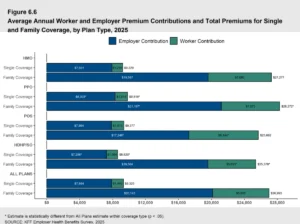

Supporting Data: The Competitive Edge of Supplemental Coverage

The shift toward robust ancillary offerings is backed by compelling data. According to the PeopleKeep by Remodel Health’s Employee Benefits Survey, the vast majority of the workforce—over four-fifths—prioritizes benefits over a marginal increase in base pay. This sentiment is particularly strong among Millennial and Gen Z workers, who often prioritize work-life balance and mental health support.

Furthermore, industry data suggests that companies offering a wide array of ancillary benefits see a 25% higher retention rate compared to those offering only basic medical insurance. For small to mid-sized enterprises (SMEs), these benefits act as an equalizer. While an SME may not be able to match the six-figure salaries offered by Silicon Valley giants, they can compete by offering high-touch, flexible benefits like Health Reimbursement Arrangements (HRAs) and specialized stipends that cater to the individual.

Deep Dive into Popular Ancillary Offerings

To understand the strategic value of these benefits, one must examine the specific protections they provide and why they resonate with today’s workforce.

Life and Disability Insurance

Group life insurance remains a cornerstone of ancillary packages. It provides a death benefit to an employee’s beneficiaries, ensuring financial stability for families in the event of a tragedy. Similarly, short-term and long-term disability insurance protects an employee’s income if they become unable to work due to illness or injury. These benefits are highly valued because they are significantly more affordable when purchased through an employer than on the individual market.

Critical Illness Insurance

As medical costs for chronic conditions and emergencies skyrocket, critical illness insurance has become a vital safety net. These policies provide a lump-sum payment upon the diagnosis of specific conditions such as cancer, heart attack, or stroke. Unlike medical insurance, which pays the provider, these funds go directly to the employee to cover non-medical costs, such as mortgage payments or transportation to treatment centers, during their recovery.

The Pet Insurance Boom

One of the fastest-growing ancillary benefits is pet insurance. With over 65% of U.S. households owning a pet, many employees view their animals as family members. Veterinary costs have risen alongside human medical costs, making pet insurance a high-perceived-value benefit. Because most pet insurance plans operate on a reimbursement model, employees have the flexibility to choose any licensed veterinarian, adding a layer of convenience that fits the modern lifestyle.

The Strategic Implementation of HRAs and Stipends

Perhaps the most significant innovation in the benefits space is the rise of Health Reimbursement Arrangements (HRAs). These are employer-funded, tax-advantaged accounts that reimburse employees for qualified medical expenses.

- Group Coverage HRA (GCHRA): Also known as an integrated HRA, this is used alongside a traditional group health plan. It allows employers to opt for a lower-cost, high-deductible health plan (HDHP) while using the HRA to reimburse employees for the resulting out-of-pocket costs, such as deductibles and co-pays.

- Individual Coverage HRA (ICHRA): This allows employers to move away from managing a group plan entirely. Instead, they provide employees with a tax-free monthly allowance to purchase their own individual health insurance on the open market. This provides maximum flexibility for the employee and cost predictability for the employer.

- Employee Stipends: Unlike HRAs, stipends are generally taxable but offer the ultimate in flexibility. Employers can provide wellness stipends for gym memberships, mental health apps, or even "lifestyle stipends" that cover anything from childcare to continuing education.

Official Responses and Industry Sentiment

Benefits experts and HR consultants increasingly argue that the "benefits gap" is where the battle for talent is won or lost. "The modern worker expects their employer to care about their holistic well-being," says a leading analyst at Remodel Health. "When an employer provides an HRA or a wellness stipend, they are sending a signal that they understand the employee’s unique financial and physical challenges."

Legal experts also note that the tax advantages of these structures are a win-win. By utilizing HRAs, businesses can deduct reimbursements as a business expense, while employees receive the money tax-free. This efficiency allows for a "hidden raise" that doesn’t increase the payroll tax burden for the company.

Broader Impact and Economic Implications

The proliferation of ancillary benefits has broader implications for the national economy and public health. By providing coverage for dental, vision, and mental health, employers are contributing to a more preventative healthcare model. Employees with access to these benefits are more likely to seek early intervention, which reduces long-term healthcare costs and decreases absenteeism.

Furthermore, the rise of portable benefits like the ICHRA could signal a long-term shift in the American healthcare landscape. If more employers move toward reimbursement models, the link between employment and a specific insurance carrier may weaken, potentially leading to a more competitive and transparent individual insurance market.

Conclusion: The Future of the Workplace

In conclusion, ancillary benefits have evolved from "extra" features to the backbone of a modern talent strategy. By filling the gaps left by traditional medical insurance, these benefits provide a safety net that addresses the physical, financial, and emotional needs of the workforce. Whether through life insurance, critical illness protection, or flexible HRAs, the move toward supplemental coverage reflects a broader societal shift toward valuing the individual. For organizations looking to thrive in a competitive landscape, the question is no longer whether to offer ancillary benefits, but how quickly they can implement a package that meets the sophisticated demands of today’s employees. Through the intelligent administration of software-driven benefits like those provided by PeopleKeep, even the smallest businesses can now offer a world-class benefits experience.