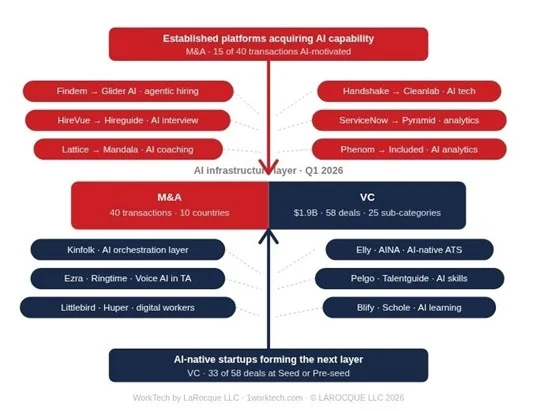

The global HR and work tech markets are undergoing a profound structural reorganization, as evidenced by the significant capital movements and strategic acquisitions tracked in the first quarter of 2026. With $1.9 billion in venture investment flowing into WorkTech and 40 tracked mergers and acquisitions (M&A) transactions, the landscape is reshaping at an accelerated pace. This dynamic shift is not merely a future projection for vendors and investors; it is an immediate reality for Chief Human Resources Officers (CHROs) whose organizations rely heavily on these evolving platforms. The traditional reactive approach to HR technology procurement is now obsolete, replaced by an imperative for proactive market intelligence and strategic foresight. Those who wait for vendor briefings will find themselves already navigating a landscape largely defined by decisions made in boardrooms and deal negotiations far removed from their immediate purview.

A Market in Flux: The Q1 2026 Snapshot

The first quarter of 2026 witnessed substantial activity, signaling a market that is both consolidating and innovating. The $1.9 billion in venture investment, while perhaps not reaching the dizzying peaks of pandemic-era funding surges, represents a focused allocation of capital towards foundational infrastructure and early-stage innovation. This investment, coupled with 40 M&A transactions, paints a clear picture: the HR technology ecosystem is building from both ends, with established players acquiring capabilities and nascent startups securing seed funding for disruptive solutions. This dual-pronged evolution is indicative of a market striving for maturity, driven by the increasing complexity of workforce management, the pervasive influence of artificial intelligence, and the strategic importance of human capital in a competitive global economy.

Historically, the HR technology market has evolved through phases, from rudimentary payroll systems in the mid-20th century to the rise of Human Resources Information Systems (HRIS) in the 1980s, followed by the internet-driven boom of integrated Human Capital Management (HCM) suites in the early 2000s. The last decade saw an explosion of "best-of-breed" point solutions, offering specialized functionalities in areas like talent acquisition, learning, and employee engagement. However, the Q1 2026 data suggests a decisive pivot back towards integration, but with a critical difference: this integration is largely driven by strategic acquisitions rather than organic development. This trend is not accidental; it reflects a growing demand from enterprises for more unified data, streamlined workflows, and a cohesive employee experience, all while navigating a rapidly changing regulatory and technological environment.

HCM Platforms Consolidate the HR Tech Stack

Perhaps the most significant revelation from Q1 2026 is not a financial figure, but a strategic direction: the aggressive expansion of HCM platforms beyond their traditional core functionalities. A striking five out of eight cross-category acquisitions tracked this quarter involved an HCM platform extending its reach into adjacent categories such as recruiting, talent management, rewards, and AI sourcing. This pattern is a continuation of a trend observed over several years, where HCM platforms consistently absorb approximately 80% of Work Tech capital quarter after quarter. Now, they are leveraging this capital advantage to acquire and integrate specialized capabilities that were once the domain of independent point solutions.

For instance, Viventium’s acquisition of an Applicant Tracking System (ATS) and VensureHR’s move to acquire an AI matching platform are not isolated incidents but represent a concerted strategy to offer comprehensive, end-to-end solutions. This trend suggests a re-evaluation of the long-standing "suite versus best-of-breed" debate, with major HCM players effectively "eating" the HR tech stack. Their motivation is clear: to become the single source of truth for all HR data, offering seamless integration, simplified vendor management, and a unified user experience.

The implications for CHROs are immediate and profound. The carefully curated ecosystem of independent recruiting, benefits, learning, and performance platforms, each selected for its specific merits and integrated with meticulous effort, may soon find themselves acquisition targets for the organization’s primary HCM vendor. This is not mere conjecture; it is the observable outcome of current transaction data. Therefore, the pertinent question for CHROs to pose to their HCM vendors today transcends typical product roadmap discussions. Instead, the focus must shift to inquiries about potential acquisition plans and the resultant impact on existing contracts, data portability, and service level agreements. Understanding these strategic moves before they materialize is paramount to maintaining control over the HR technology landscape. Industry analysts, like those at Forrester and Gartner, have been hinting at this consolidation for years, emphasizing the importance of a robust integration strategy. The Q1 2026 data confirms this foresight, indicating that the pace of integration is now accelerating through M&A.

AI’s Acquisition-Driven Ascent in HR Technology

The transformative potential of Artificial Intelligence (AI) has been a dominant theme across industries, and HR technology is no exception. However, Q1 2026 data reveals a crucial insight into how AI capabilities are truly entering the HR tech stack: predominantly through acquisition rather than organic product updates. Out of the 40 M&A transactions tracked, at least 15 explicitly cited AI capability as the primary rationale. This acquisition-first approach signifies a rapid deployment strategy, where vendors are buying specialized AI companies for their foundational technology, talent, and proven algorithms, rather than spending years developing these capabilities in-house.

This mechanism is critical for CHROs to grasp. The AI features that will eventually appear in their current vendor’s interface in the coming months are likely the result of strategic acquisitions made today. Companies like Handshake, which acquired an AI company for its core technology and expert team, are not merely adding a new "feature" but integrating a fundamental capability that will power the next generation of their platform. Similarly, Findem’s acquisition of Glider AI for agentic hiring, HireVue’s integration of Hireguide for AI interview intelligence, and Lattice’s purchase of Mandala for AI coaching all underscore this trend. These acquired capabilities will be rebranded, integrated, and presented as seamless enhancements, often without explicit mention of their acquisition origin. By the time these AI-powered functionalities are showcased in product demos, the strategic decision to acquire them would have been made a year prior, precluding any direct input from the end-user CHROs.

The harder truth is that the AI transformation of the HR tech stack is being designed in boardrooms and through complex deal negotiations to which CHROs are not privy. This underscores the urgent need for HR leaders to move beyond passively consuming vendor roadmaps. Those CHROs who actively track the investment and M&A landscape are uniquely positioned to ask the right, forward-looking questions before critical decisions are finalized, thereby influencing the trajectory of their organization’s AI adoption in HR rather than merely reacting to it. The strategic implications of this "buy, don’t build" AI approach extend to faster innovation cycles for vendors but also necessitate heightened due diligence from CHROs regarding data privacy, algorithmic bias, and the ethical deployment of AI within their organizations.

Critical Categories Undergoing Consolidation

The Q1 2026 data illuminates four specific sub-categories within HR technology that are experiencing active consolidation, each with distinct implications for how CHROs should manage their vendor relationships:

-

Assessment: This category is witnessing a fascinating, multi-directional absorption. Acquisitions in Q1 came from an ATS platform, a talent management (TM) suite, a background check company, and a talent intelligence platform simultaneously. This fragmented consolidation indicates that no single player is dominating the assessment space; rather, assessment capabilities are being integrated into various adjacent platforms, each driven by different strategic interests. For a CHRO, this fragmentation presents a challenge: if an assessment vendor is acquired, the priorities of the acquiring platform—be it a broader talent suite or a specialized background check provider—may not align with the specific needs or long-term vision of the acquiring organization. This makes understanding contractual protections, particularly concerning data ownership, integration continuity, and service level agreements post-acquisition, more critical than ever. The increasing emphasis on objective, bias-free assessment tools, often powered by AI, makes this category a vital component of fair hiring practices, further complicating the acquisition landscape.

-

Learning: The learning technology landscape presents a complex narrative of simultaneous consolidation and fragmentation. On one hand, growth-stage companies like Preply secured significant funding ($150 million), while established players such as Docebo acquired skills intelligence companies, and Perceptyx expanded into learning platforms. This top-down consolidation suggests a move towards integrated learning and development ecosystems. On the other hand, the emergence of numerous early-stage AI learning companies, raising seed rounds averaging under $4 million, indicates a fragmentation at the innovative edge. These startups are likely focusing on highly specialized AI-driven learning experiences, personalized content delivery, or advanced skill gap analysis. The practical implication for CHROs is significant: the learning platform that met organizational needs three years ago might not be adequate in two years, especially given the rapid evolution of skills required in the modern workforce. Furthermore, the optimal replacement solution may not even exist yet in its mature form. This necessitates a forward-looking strategy that anticipates the convergence of established learning management systems with agile, AI-native specialists.

-

Benefits: Q1 2026 saw eight venture deals in the benefits sector, making it the most distributed investment activity across all sub-categories. Capital is flowing into a wide spectrum of point solutions, including healthcare navigation, AI benefits administration, housing benefits, Employee Assistance Programs (EAPs), and financial wellness platforms. This influx of investment suggests that the benefits technology landscape is poised to become more complex before it simplifies. Employers are under increasing pressure to offer competitive and personalized benefits packages to attract and retain talent, driving demand for innovative solutions. However, managing a fragmented array of benefits vendors can create administrative burdens and a disjointed employee experience. For CHROs, understanding which vendors are well-capitalized—and thus likely to innovate and grow—versus those that might be attractive acquisition targets is no longer an IT function but a core strategic competency. This requires deep market awareness and the ability to project future trends in employee welfare and support.

-

Job Boards/Sourcing: The traditional job board as a standalone sourcing channel is undergoing a quiet but fundamental transformation. The platforms attracting significant investment and acquisition activity in Q1 2026 are not conventional job boards; they are sophisticated "marketplaces" that seamlessly combine sourcing with vetting, screening, scheduling, and matching capabilities. Examples include Paraform, which raised $40 million to build a recruiter marketplace with embedded workflow, and Juicebox, which secured $80 million for its AI sourcing capabilities and is poised to extend into core workflow management. Carefam, connecting hiring to agents, further exemplifies this shift. The consolidation occurring within traditional job boards is less impactful than the emergence of these entirely new sourcing infrastructures. If an organization’s recruiting stack was designed primarily around broad-based job board distribution, the more urgent question now is whether it is architected to connect with this next generation of sourcing infrastructure, which is being built in real-time and bears little resemblance to its predecessors. This trend necessitates a re-evaluation of an organization’s entire talent acquisition strategy, moving towards more intelligent, data-driven, and integrated sourcing channels.

Navigating the New Landscape: A Proactive CHRO Imperative

The traditional CHRO approach to HR technology—characterized by reactive vendor evaluations upon contract expiry, initiating RFPs only when pain points become acute, and relying solely on analyst briefings for market context—is no longer sustainable. This model was adequate when market movements were slow and predictable, but it is woefully insufficient in the current environment of rapid structural reorganization. Q1 2026 data serves as a powerful signal, indicating a definitive direction that will only become clearer and more consequential as the year progresses. CHROs who act decisively on this intelligence are not those who merely read a quarterly report and move on; they are those who embed continuous market intelligence into their operational framework year-round.

Three key actions are imperative for CHROs based on the insights from Q1 2026:

-

Map Your Current Stack Against M&A Activity: Every platform currently in use by an organization is either an acquirer, a likely acquisition target, or both. Understanding this positioning is critical. This knowledge fundamentally alters negotiation strategies, informs the inclusion of specific clauses in contracts (e.g., change of control, data ownership, service continuity post-acquisition), and shapes considerations around data portability. Proactively identifying potential acquisition targets within your vendor ecosystem allows for strategic planning, mitigating risks associated with service disruption, integration challenges, and potential vendor lock-in. This exercise should be a continuous process, not a one-time event.

-

Get into the Capital Signal Earlier: Investment data is a powerful predictor of future product roadmaps, often signaling vendor priorities 18 months before they manifest in tangible product updates. The fact that the benefits category is receiving more capital than any other sub-category indicates a forthcoming surge in innovation, a wider array of vendor options, and increased complexity. CHROs must prepare for this influx by understanding emerging trends in employee wellness and personalized benefits. Similarly, the bifurcation of the learning market into large-scale platforms and AI-native specialists means that a current learning vendor, while perhaps effective for general L&D, may not be the optimal solution for future AI-driven skill development. By monitoring venture capital flows and strategic investments, CHROs can anticipate market shifts and align their long-term HR technology strategy accordingly.

-

Treat AI as an Acquisition Strategy, Not a Feature: The advanced AI capabilities that will appear in vendor platforms over the next 6-12 months were largely acquired in Q1 2026. CHROs can, and must, track these acquisitions. WorkTech, among other specialized publications, provides this crucial data. By understanding which AI firms have been acquired, what specific capabilities they bring (e.g., generative AI for content creation, predictive analytics for talent forecasting, agentic AI for autonomous workflows), and how these acquisitions fit into the broader strategy of their current vendors, CHROs can engage in more informed, proactive conversations. This level of insight allows them to walk into vendor meetings already understanding the newly acquired capabilities and their potential implications for their organization’s HR strategy, rather than passively receiving information. This proactive stance enables CHROs to influence the design and implementation of AI within their HR tech stack, ensuring it aligns with their organizational values, ethical guidelines, and strategic objectives.

The HR technology market is engaged in a profound strategic conversation, articulated through term sheets, acquisition announcements, and investment theses. CHROs who understand this language—who speak in terms of capital signals and platform strategy—are the ones who will actively shape what their organizations acquire and deploy, rather than simply accepting what the market delivers. The data is openly available; the critical question is whether CHROs are leveraging it to drive proactive, informed decision-making in this rapidly evolving landscape.