The landscape of American manufacturing in July presents a dichotomy: robust demand for goods and services continues to fuel optimism about current business conditions, yet a palpable sense of caution is creeping into the outlook for the next twelve months. While U.S. manufacturers overwhelmingly report that demand is stronger than it was a year ago, a softening 12-month outlook suggests that chief executive officers are tempering their optimism for the future. This shift marks a notable recalibration of expectations, moving away from the more expansive optimism seen in prior months towards a more measured and perhaps realistic appraisal of the economic horizon.

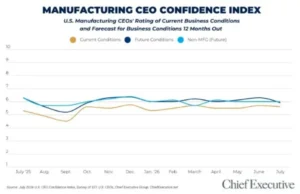

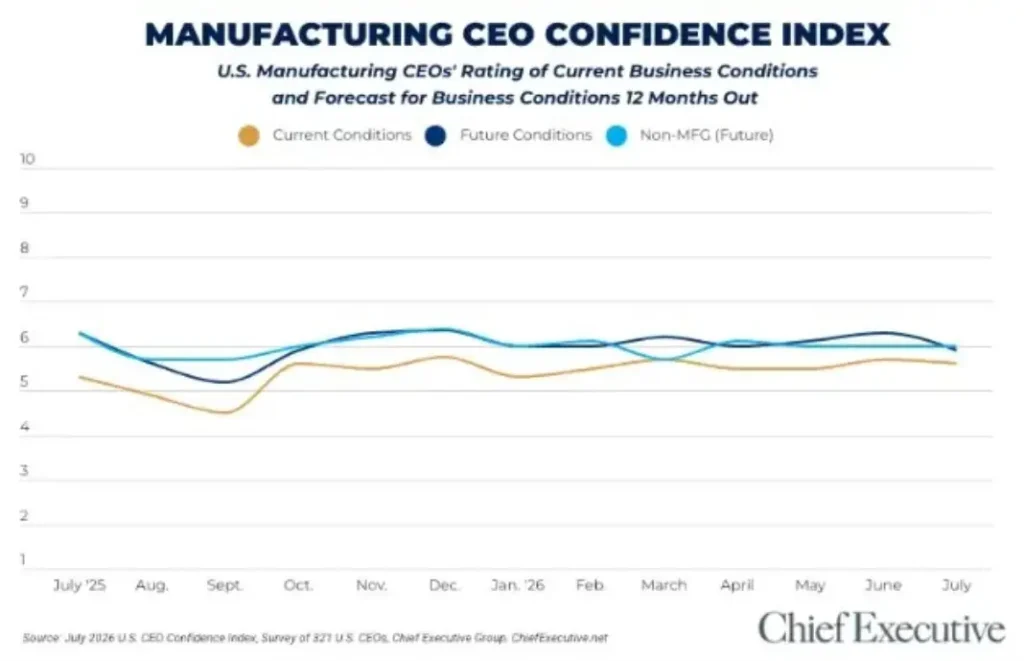

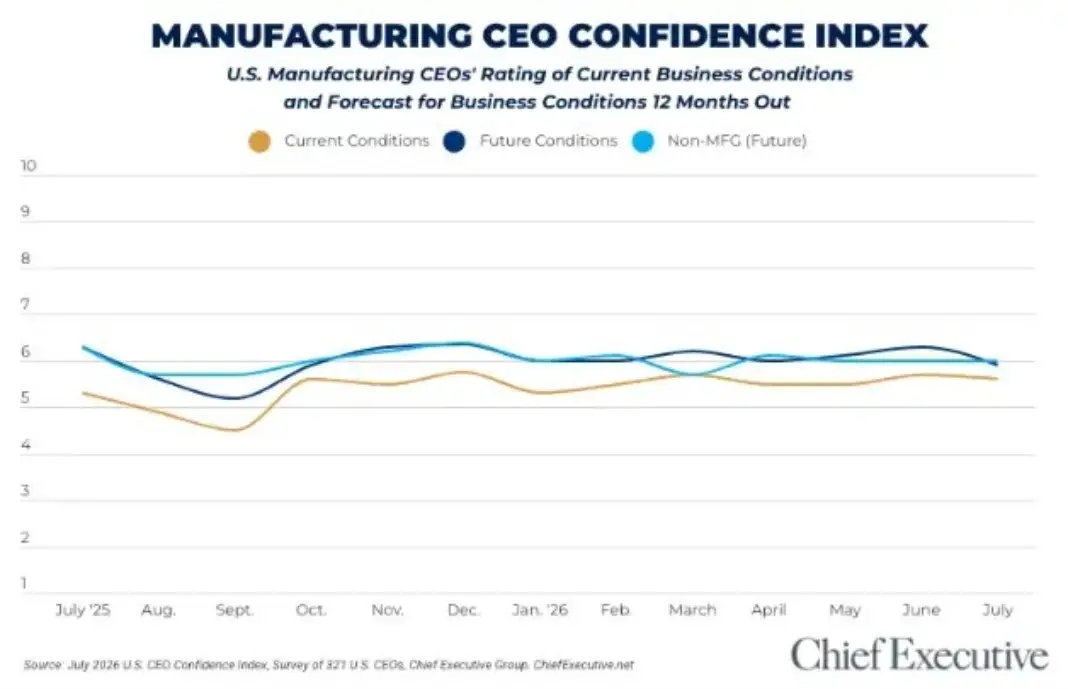

The latest CEO Confidence Index, a quarterly survey conducted by Chief Executive among 321 U.S. CEOs, reveals that manufacturers rated current business conditions at a 5.6 out of 10 in early July. This score, on a scale where 1 signifies "Poor" and 10 represents "Excellent," represents a marginal 2 percent decline from the previous month. However, it remains among the sector’s strongest ratings for the year, underscoring a persistent resilience in the face of evolving economic pressures. A historical review of this index shows a remarkable stability in current confidence ratings, which have hovered consistently between 5.5 and 5.7 out of 10 since February of this year. This suggests that, despite reservations about the future, the manufacturing sector’s assessment of its present operating environment has remained largely unchanged over the past six months, indicating a solid foundation built on sustained demand.

The divergence in sentiment becomes apparent when examining the forward-looking projections. Manufacturers anticipate business conditions to reach 5.9 out of 10 by this time next year, a notable 6 percent decrease from June’s more buoyant forecast of 6.3 out of 10. This decline is significant, marking the sector’s lowest year-ahead forecast of the year and the first time the Index has dipped below the 6.0 mark since October of the previous year. While this future outlook still signals an expected improvement over current conditions, it underscores a growing conservatism among CEOs regarding the magnitude and certainty of that future growth. This recalibration effectively erases the optimism gap that manufacturers had maintained over their non-manufacturing peers since May of the previous year. Now, manufacturers’ 5.9 forecast for the year ahead sits just below the 6.0 rating that non-manufacturing businesses have consistently reported for three consecutive months, indicating a convergence in outlook between the two broad economic sectors.

Drivers of Current Confidence and Future Concerns

The bedrock of current manufacturing confidence is overwhelmingly attributed to improving and healthy demand. CEOs across the sector report a steady stream of orders and a consistent market for their products and services. This sustained demand acts as a powerful buffer against other emerging headwinds. However, this positive demand picture is juxtaposed with significant concerns that are shaping the more cautious 12-month outlook. Chief among these are the increasing regulatory burdens, rising operational costs, and the perceived instability of rapidly shifting policy landscapes.

Greg Immell, CEO of Saporito Finishing, a small-sized industrial manufacturing firm, articulated this sentiment: "Revenues are increasing as we see increased demand; however, healthcare, energy, and wages have increased. The battle is to improve efficiencies to protect margins." His statement highlights the delicate balancing act manufacturers face: leveraging strong demand to drive revenue while simultaneously grappling with escalating input costs that threaten profitability. The imperative to enhance operational efficiencies has never been greater, as companies strive to absorb rising expenses without passing the full burden onto consumers, which could dampen the very demand they are currently benefiting from.

The impact of policy inconsistency was further emphasized by John Evans, president of a small-sized lumber manufacturing firm. He stated, "If we can keep the same tariff policies for more than a month, I think the industry will be confident to make plans longer than a few weeks." This concern points to the disruptive nature of unpredictable trade policies and regulations. For manufacturers who rely on long-term planning for supply chain management, capital investments, and workforce development, a volatile policy environment creates significant uncertainty, hindering their ability to commit to ambitious future strategies. This sentiment is echoed by other industry leaders who cite "higher costs driven by geopolitics [and] interest rates," painting a picture where strong demand is making it increasingly challenging to capitalize on due to escalating external cost pressures. The interplay between robust demand and rising costs, compounded by policy flux, forms the complex economic reality for today’s U.S. manufacturing sector.

Economic Outlook: A Mixed but Improving Picture

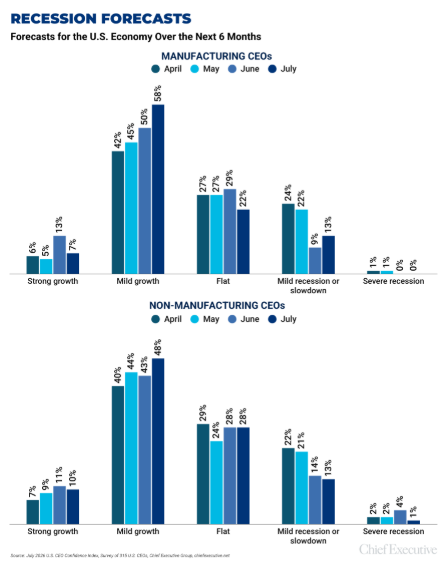

Despite the softening 12-month forecast for their own sector, manufacturing CEOs’ expectations for the broader U.S. economy have continued to improve throughout July. A substantial 65 percent of manufacturers now forecast some form of economic growth over the next six months, an increase from 63 percent in June. This marks the third consecutive monthly improvement in economic growth expectations, indicating a general sense of optimism about the national economic trajectory. However, this optimism is characterized by a trend toward more modest growth projections. The proportion of CEOs forecasting "significant" economic growth has fallen by nearly 50 percent compared to the previous month, suggesting a shift towards anticipating incremental gains rather than substantial economic leaps.

Concurrently, the proportion of manufacturers forecasting some form of recession has seen a slight uptick, rising from 9 percent in June to 13 percent in July. While this increase is notable, it remains within a range that many economists would consider manageable and indicative of a resilient, albeit not invulnerable, economy.

In a comparative analysis, manufacturers continue to exhibit a more optimistic view of the national economy than their non-manufacturing counterparts. Only 58 percent of non-manufacturing CEOs forecast economic growth for the next six months. Interestingly, the concerns of recession among the non-manufacturing sector have softened somewhat, decreasing by 22 percent since June, suggesting a degree of stabilization in their outlook, even if overall growth expectations are lower.

Demand Dynamics: The Unwavering Engine of Manufacturing Resilience

The persistent strength of demand remains the most significant factor underpinning the resilience of the manufacturing sector. According to the survey data, more than half of manufacturers (52 percent) report that demand for their products and services is higher today than it was one year ago. A notable 18 percent of these respondents describe this increase in demand as "significant," highlighting a powerful upward trend for a substantial portion of the industry. Conversely, only 22 percent of manufacturers indicate that demand has declined over the past year, underscoring the widespread positive trajectory.

Manufacturers are notably more bullish on the increase in demand compared to their non-manufacturing peers. Among non-manufacturers, only 12 percent describe a "significant" change in demand, indicating that while demand may be growing, the intensity of that growth is perceived differently across sectors. This divergence suggests that the manufacturing sector, in particular, is experiencing a pronounced surge in customer interest and purchasing activity, which is a critical driver of its current strong performance.

Corporate Forecasts: Rising Operational Expenditures and Evolving Strategies

The outlook for corporate forecasts within the manufacturing sector presents a mixed picture, with a significant concern emerging around operational expenditures. A staggering 77 percent of manufacturers foresee increases in their operational expenditures. This figure represents a substantial 60 percent increase from June, a month during which manufacturers had expressed unusually optimistic sentiments regarding the burden of organizational costs. This sharp rise in anticipated expenditure increases suggests a significant shift in the cost environment, potentially driven by a confluence of factors including supply chain disruptions, commodity price fluctuations, labor costs, and energy prices.

This surge in expected cost increases is likely contributing to the tempered optimism for the year ahead. As operational costs climb, manufacturers face increased pressure to maintain profit margins, which can influence investment decisions, hiring plans, and pricing strategies. The need to manage these rising costs effectively will be a defining challenge for the sector in the coming months, requiring strategic adjustments to improve efficiencies, optimize supply chains, and potentially pass on some of the increased costs to consumers, albeit cautiously given the current demand environment.

Historical Context of the CEO Confidence Index

The CEO Confidence Index, compiled by Chief Executive Group since 2002, has served as a critical barometer of the economic sentiment among U.S. business leaders. The survey regularly polls hundreds of CEOs across organizations of all types and sizes, providing valuable insights into their confidence levels regarding both current and future business environments. By tracking observations across various economic and business components, the Index offers a nuanced understanding of the challenges and opportunities shaping the corporate landscape. This long-standing data set allows for historical comparisons and trend analysis, illuminating how perceptions of economic health and future prospects evolve over time. Previous reports from the Index have highlighted periods of strong growth, periods of economic contraction, and the persistent factors that influence CEO decision-making, such as regulatory environments, technological advancements, and global economic shifts. The current July report, with its emphasis on the divergence between present strength and future caution, adds another layer to this ongoing narrative of American business sentiment.

Broader Implications and Expert Analysis

The current sentiment among U.S. manufacturers, characterized by strong current demand but a cautious outlook, carries significant implications for the broader economy. The sustained demand for manufactured goods is a positive indicator, suggesting continued consumer and business spending. This demand fuels job creation, drives innovation, and contributes to overall economic growth. However, the growing concerns about rising costs and policy uncertainty present potential headwinds.

If rising operational costs are not effectively managed, manufacturers may be forced to slow production, reduce investments, or increase prices, which could, in turn, dampen consumer demand and slow economic momentum. The impact of policy instability, particularly concerning trade and regulations, can create a chilling effect on long-term investment decisions. Businesses are less likely to commit capital to expansion or new projects when the regulatory landscape is unpredictable. This can hinder the sector’s ability to innovate and compete on a global scale.

Industry analysts suggest that manufacturers will need to focus on strategies that enhance their resilience and adaptability. This includes diversifying supply chains to mitigate risks associated with geopolitical events, investing in automation and technology to improve efficiency and reduce labor costs, and proactively engaging with policymakers to advocate for stable and predictable regulatory frameworks. The current environment underscores the importance of agility and strategic foresight for U.S. manufacturers navigating a complex and dynamic global marketplace. The ability to leverage current demand while proactively addressing future challenges will be crucial for sustained success.