The landscape for U.S. manufacturing CEOs brightened considerably in June, as a confluence of robust order books, diminishing concerns about an impending recession, and enhanced access to new markets bolstered confidence. This surge in optimism, however, did not entirely eclipse the persistent headwinds of cost pressures and ongoing geopolitical uncertainties that continue to cast a shadow over the sector. The latest Chief Executive CEO Confidence Index, a key barometer of sentiment among business leaders, reveals a discernible shift from the cautious apprehension that characterized the early part of the year.

Since the dawn of 2024, manufacturing leaders have consistently articulated a dual perspective: grappling with immediate, tangible pressures while simultaneously holding a cautious, albeit growing, optimism for the future. June’s data indicates that this perceived gap is beginning to narrow, suggesting a more unified and positive outlook is taking root.

Key Findings from the June CEO Confidence Index

The Chief Executive CEO Confidence Index, a survey conducted among 315 U.S. CEOs on June 2-3, offers a granular view of this evolving sentiment. Manufacturers rated their current business conditions at an average of 5.7 out of 10, where 1 signifies "Poor" and 10 represents "Excellent." This score marks a significant 4 percent increase from May and, critically, represents the first upward revision in manufacturers’ assessment of current conditions since March. This upward trend suggests that the pressures that weighed on sentiment during the spring months may be starting to abate, allowing for a more favorable perception of the present economic environment.

The optimism extends beyond the immediate present, with manufacturing CEOs expressing a more upbeat outlook for the year ahead. Projections for business conditions 12 months from now reached an average of 6.3 out of 10, a notable increase from May’s 6.0. This marks the first instance in several months where manufacturers have simultaneously improved their assessments of both current conditions and their future prospects, indicating a more comprehensive and sustained wave of positive sentiment.

Manufacturing Sector Outpaces Non-Manufacturing Peers

Further underscoring the sector’s growing buoyancy, manufacturers have consistently expressed more optimism about the future than their non-manufacturing counterparts since April. This trend widened in June, with manufacturers’ 12-month outlook reaching 6.3 out of 10, a 5 percent increase from the previous month. In contrast, non-manufacturing CEOs maintained their 12-month outlook at a steady 6.0 out of 10. This divergence highlights the manufacturing sector’s increasing confidence, even within a broader economic climate marked by persistent uncertainty.

Drivers of Improved Sentiment: Demand, Orders, and Stability

When probed about the catalysts behind this resurgence in confidence, a recurring theme among manufacturing CEOs was the robust nature of current demand, the health of their order books, and tangible signs of greater stability within their own businesses and the end markets they serve.

Jason Stanczyk, CEO of Equipment Development Company, a small, family-owned industrial manufacturing firm, articulated this positive trend: "Orders are up over 12 months ago. The industries we serve are predicting growth over the next 24 months. We continually find the right talent for the fair market salaries we pay." This statement encapsulates a multifaceted improvement, touching upon order flow, forward-looking industry forecasts, and the critical element of talent acquisition.

Peter Ensch, CEO of Sani-Matic, a mid-sized industrial goods manufacturer, described a similar transition from a period of uncertainty to a phase of focused execution. He noted, "I believe manufacturing is entering a phase of stability as business leaders have grown accustomed to the constant chaos of the current administration combined with pent-up demand, leading to projects being released." This perspective suggests that businesses have adapted to prevailing complexities, enabling them to capitalize on pent-up demand and move forward with planned projects.

Persistent Challenges: Cost Pressures and Geopolitical Uncertainty

Despite the encouraging uptick in confidence, the recovery remains uneven. For a significant segment of manufacturers, entrenched cost pressures, the lingering uncertainty surrounding tariffs, regulatory burdens, and ongoing supply chain disruptions continue to exert downward pressure on profit margins and dampen customer demand.

Katie Malnight Meisinger, president of RELY Contract Manufacturing, highlighted the impact of global events: "Geopolitics is driving up fuel and raw material prices which is eating into margins, dampening demand and/or causing customers to push out timelines." This sentiment underscores how external geopolitical factors can have a direct and material impact on the operational and financial health of manufacturing enterprises.

Manufacturers with substantial exposure to government contracts also cited policy ambiguity and regulatory complexities as significant points of pressure. Specific concerns were raised regarding "government research funding policies" and "constant supply chain disruptions," which continue to complicate strategic planning and operational execution.

Economic Outlook: A Reversal of Springtime Pessimism

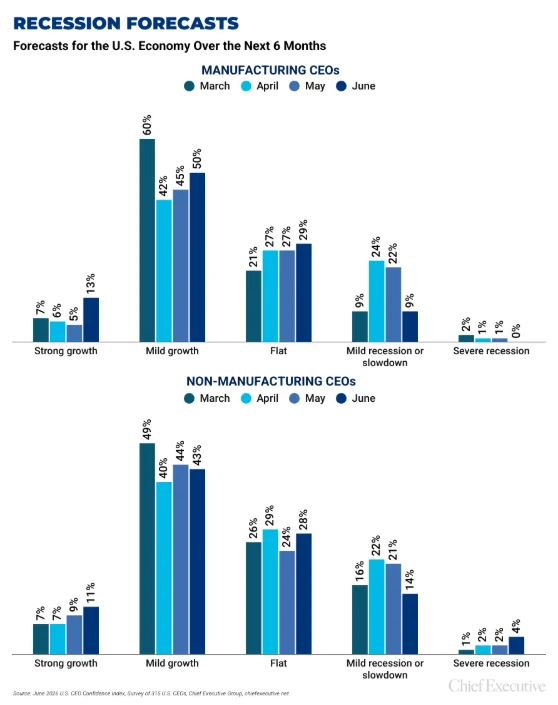

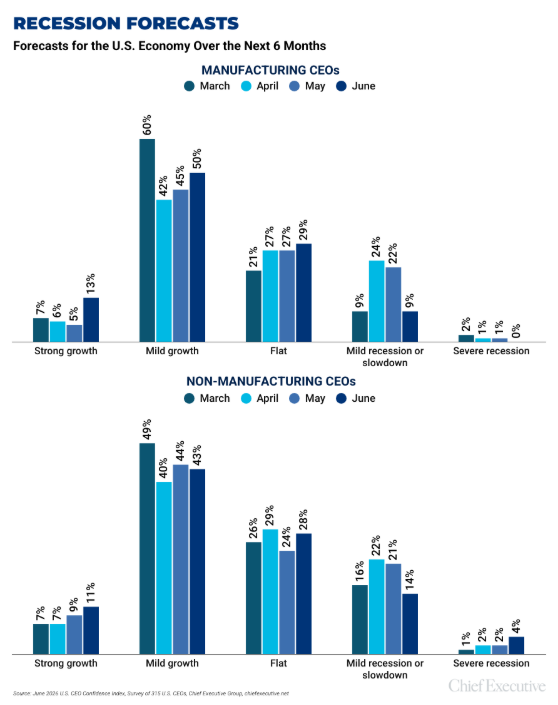

The broader economic outlook for manufacturing CEOs experienced a sharp improvement in June, effectively reversing much of the decline observed earlier in the spring. After reaching a peak in March, when a substantial 67 percent of manufacturers anticipated U.S. growth by year-end, this figure dipped to 48 percent in April and 50 percent in May. In June, however, the sentiment rebounded significantly, with 63 percent of manufacturers once again forecasting some form of economic growth before the close of the year.

This renewed optimism places manufacturers ahead of their non-manufacturing peers, among whom only 54 percent expect the U.S. economy to grow over the same period. This divergence could be attributed to a combination of factors, including improving demand dynamics, a renewed focus on reshoring initiatives, and domestic capacity expansion, all occurring amidst ongoing tariff and regulatory uncertainties.

Easing Recession Fears

Recessionary anxieties also appear to be subsiding among manufacturers. While the proportion of non-manufacturing CEOs forecasting a severe recession within the next six months has seen a steady increase since March, reaching 4 percent in June, notably, no manufacturing respondents indicated such a concern in the latest survey. This absence of recessionary forecasts from the manufacturing sector’s leadership is a significant indicator of their perceived resilience and the sector’s ability to navigate potential economic downturns.

Diversification and Market Expansion: Pillars of Future Growth

Beyond improved demand, manufacturing CEOs are increasingly highlighting diversification and market expansion as crucial strategies for growth in an inherently volatile global environment. A substantial nearly three-quarters of manufacturing CEOs reported that their companies have expanded into new sectors, customer categories, geographic markets, or identified new use cases for their existing products and services over the past five years.

This strategic diversification is anticipated to remain a cornerstone of competitiveness. Looking ahead over the next three to five years, an overwhelming 82 percent of manufacturers deem diversification as either critical or important to their company’s ability to grow and maintain a competitive edge. Only a negligible 1 percent of respondents indicated that diversification is not a priority, underscoring its widespread recognition as a vital strategic imperative.

Corporate Forecasts: A Picture of Cautious Optimism

Despite the overall improvement in confidence, corporate forecasts from manufacturing CEOs presented a more nuanced picture in June, suggesting a degree of caution in translating heightened sentiment into aggressive expansion plans. While the general mood is positive, specific investment and hiring intentions remain more tempered, reflecting a strategic approach to growth in an unpredictable economic climate.

Background and Context: Navigating a Complex Economic Landscape

The June survey results arrive at a critical juncture for the U.S. manufacturing sector. The period leading up to this assessment was marked by a series of economic indicators that painted a complex picture. Inflationary pressures, while showing some signs of moderation, remained a concern, impacting input costs and consumer spending. Geopolitical tensions, particularly in Eastern Europe and the Middle East, continued to disrupt global supply chains and contribute to energy price volatility. Domestically, the Federal Reserve’s monetary policy adjustments aimed at taming inflation also introduced a degree of uncertainty regarding interest rates and their impact on investment and borrowing costs.

Against this backdrop, the resilience and adaptability of U.S. manufacturers have been put to the test. The sector has been a key focus for policymakers seeking to bolster domestic industrial capacity and reduce reliance on foreign supply chains. Initiatives aimed at reshoring production, investing in advanced manufacturing technologies, and developing a skilled workforce have been central to the economic agenda. The current sentiment among CEOs suggests that these efforts, coupled with the inherent strengths of the U.S. manufacturing base, are beginning to yield positive results.

Timeline of Sentiment Shifts

- Early 2024: Manufacturing CEOs consistently described a sector caught between near-term pressures and cautious optimism.

- March 2024: Peak optimism regarding year-end U.S. economic growth (67% expected growth).

- April 2024: A dip in growth expectations (48% expected growth); manufacturers began to express more optimism than non-manufacturing peers.

- May 2024: Slight recovery in growth expectations (50% expected growth); sentiment remained cautiously optimistic.

- June 2-3, 2024: Significant rebound in confidence. Current conditions rated 5.7/10 (up 4% from May). 12-month outlook rated 6.3/10 (up from 6.0 in May). 63% forecast U.S. growth by year-end. No manufacturing respondents forecast a severe recession.

Analysis of Implications: A Foundation for Future Growth?

The renewed optimism among U.S. manufacturing CEOs in June suggests that the sector is entering a more stable and potentially growth-oriented phase. The combination of strong order books and a receding fear of recession provides a solid foundation for future investment and expansion. The emphasis on diversification and market expansion is particularly noteworthy, indicating a strategic pivot towards resilience and adaptability in the face of ongoing global uncertainties.

However, the persistent challenges of cost pressures and geopolitical instability cannot be overlooked. These factors continue to represent significant risks that could temper the current positive momentum. The ability of manufacturers to effectively manage these external pressures while capitalizing on internal strengths will be crucial in determining the long-term trajectory of the sector.

The widening confidence gap between manufacturing and non-manufacturing sectors could also signal a period of outperformance for manufacturing. As global supply chains continue to recalibrate and reshoring efforts gain traction, the manufacturing sector may be uniquely positioned to benefit from these structural shifts.

Official Responses and Broader Economic Impact

While specific official responses to the June CEO Confidence Index were not detailed in the provided text, the data aligns with broader economic policy discussions. Government bodies and industry associations have consistently emphasized the importance of supporting the manufacturing sector through various initiatives, including infrastructure investment, workforce development programs, and trade policies aimed at creating a more favorable business environment. The positive sentiment reported by CEOs could be interpreted as a signal that these efforts, or the underlying economic fundamentals, are beginning to resonate.

The implications of this improved manufacturing sentiment extend beyond the sector itself. A robust manufacturing base is a key driver of job creation, technological innovation, and overall economic growth. A sustained period of optimism and investment in manufacturing could translate into higher employment rates, increased consumer spending, and a stronger, more resilient U.S. economy.

About the CEO Confidence Index

The Chief Executive CEO Confidence Index has been a reliable gauge of U.S. business leader sentiment since 2002. The index compiles data from hundreds of U.S. CEOs across various industries and company sizes, tracking their confidence in both current and future business environments. The index’s methodology involves assessing various economic and business components, providing valuable insights into the prevailing economic climate and the strategic outlook of corporate leadership. Further information and historical data can be accessed through ChiefExecutive.net.