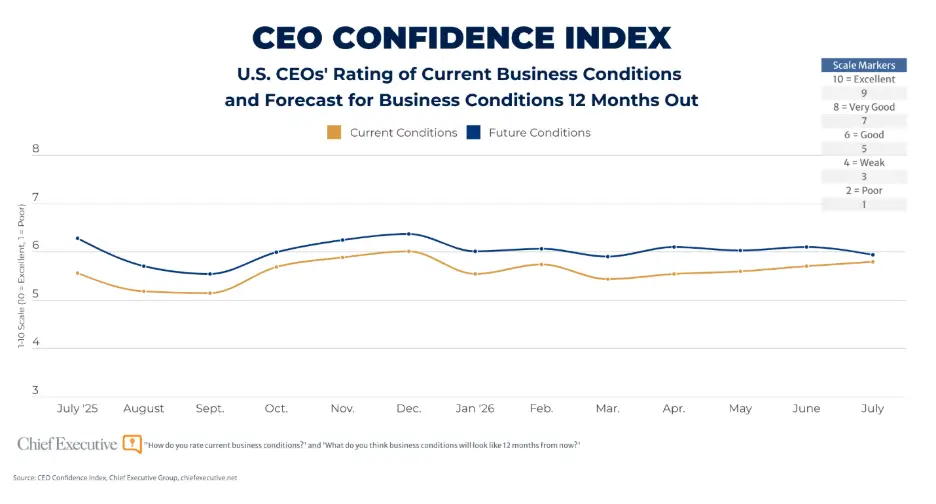

American CEOs are exhibiting a cautious optimism regarding current business conditions, yet a palpable sense of apprehension permeates their outlook for the coming year. The latest Chief Executive CEO Confidence Index, a survey conducted from July 7-9 among 321 U.S. chief executive officers, reveals that while leaders’ assessments of the present business landscape have improved for a fourth consecutive month, reaching 5.8 out of 10 – the highest reading of the year – their forward-looking projections have softened. This nuanced sentiment reflects a complex interplay of persistent cost pressures, lingering policy uncertainties, and the escalating impact of geopolitical events on corporate strategy and investment decisions.

The survey data indicates that CEOs now anticipate business conditions to reach 5.9 by this time next year, a 3 percent decrease from the 6.1 forecasted in June. While this still represents an improvement over current conditions, it falls significantly short of the average 8 percent improvement projected by CEOs each month throughout the preceding year. This shift does not necessarily signal a widespread descent into pessimism. Instead, it suggests a recalibration of expectations, with the proportion of CEOs anticipating business conditions to improve over the next 12 months declining from 47 percent to 37 percent. Concurrently, the share of leaders expecting conditions to remain stable has risen to 38 percent, while only a quarter foresee a worsening economic environment – a sentiment that has remained relatively consistent throughout 2026.

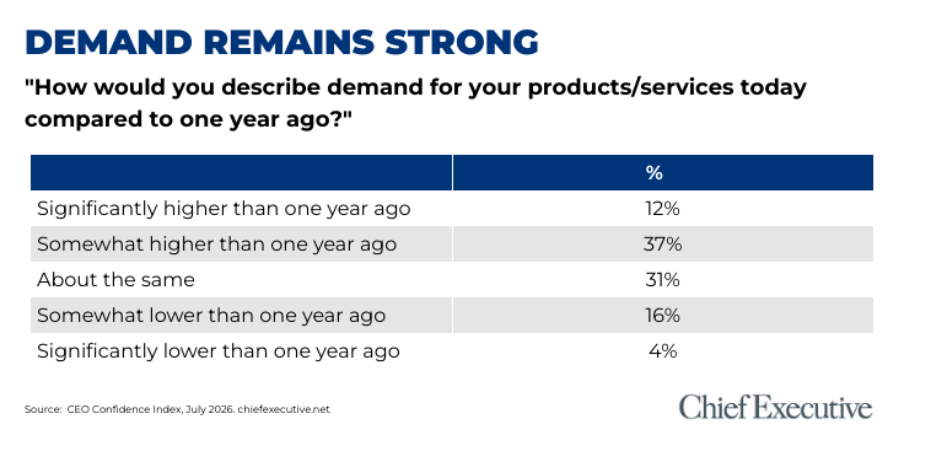

The driving force behind the current positive sentiment appears to be robust demand for products and services. Nearly half of the CEOs surveyed (49 percent) reported higher demand for their company’s offerings compared to a year ago, with an additional 31 percent noting unchanged demand. Only 20 percent reported weaker demand. Intriguingly, even among those CEOs who anticipate a decline in business conditions over the next year, a slight majority (51 percent) are currently experiencing higher demand than they did a year prior, a figure marginally exceeding that of optimists and neutral respondents (both at 48 percent).

However, this strong demand is being significantly offset by escalating cost pressures. CEOs are grappling with a multifaceted surge in expenses, citing price volatility across various sectors, escalating healthcare and energy costs, and the persistent challenge of rising wages. The difficulty in finding and retaining qualified talent further exacerbates these pressures, creating a tight labor market that drives up compensation demands.

Greg Immell, CEO of Saporito Finishing Company, an anodizing and metal finishing manufacturer based in Illinois, encapsulates this dichotomy. "Demand and revenues are increasing at our company," Immell stated. "However, healthcare, energy, and wages have increased. The battle is to improve efficiencies to protect margins." This sentiment is echoed by another anonymous CEO who observed, "Opportunities are significant, but the overall environment is very unstable right now. Challenging times."

In response to these mounting cost pressures, forward-thinking leaders are exploring innovative solutions. Robert Colescott, CEO of Southern Specialties, highlighted the transformative potential of artificial intelligence (AI) and automation. "Artificial intelligence, automation, and other digital tools provide us with opportunities to reduce costs, eliminate inefficiencies, improve decision-making, and streamline many of our business processes," Colescott remarked. This indicates a strategic pivot towards technological adoption as a means to enhance operational efficiency and safeguard profit margins amidst economic headwinds.

The U.S. Economic Outlook: A Mixed Picture

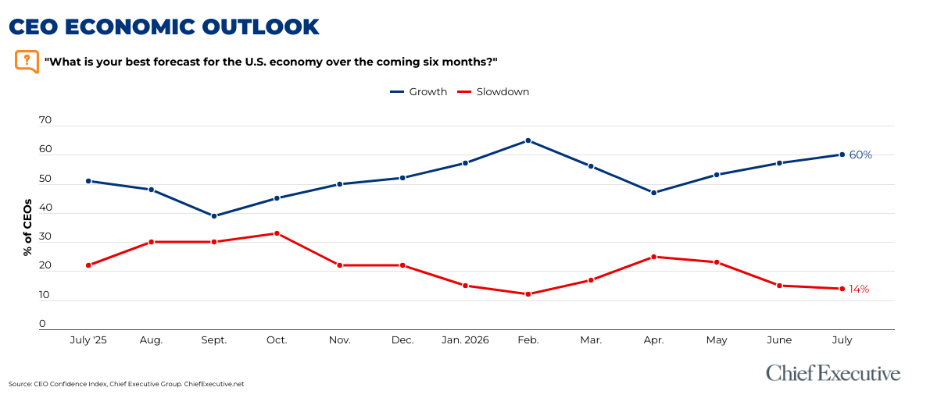

Looking ahead to the next six months, the U.S. economy is perceived as more growth-oriented than recessionary by a significant margin. Sixty percent of CEOs anticipate either strong or mild growth, while 26 percent expect the economy to remain flat. A smaller, yet concerning, 14 percent foresee a mild or severe recession. This outlook, while generally positive, is tempered by persistently elevated inflation expectations. For the fourth consecutive month, CEOs have forecasted an average inflation rate of 3.6 percent over the next 12 months, underscoring the continued prominence of pricing and cost pressures in their strategic considerations.

Corporate Forecasts: Prudence Over Expansion

Despite expectations of stronger revenues, these positive projections are not translating into more aggressive hiring or capital investment strategies. The survey reveals that 73 percent of CEOs polled anticipate higher revenues in 2026 compared to 2025, and 65 percent foresee an increase in profits. However, a concerning trend emerges when examining workforce and investment plans. The proportion of CEOs forecasting headcount reductions has risen to 22 percent from 17 percent in June, while the share planning to decrease capital expenditures has climbed to 21 percent from 17 percent in the same period.

This disconnect between revenue optimism and cautious investment signals a broader hesitancy among corporate leaders. "It is not possible to make clear investment and growth decisions in this environment," stated one CEO. "Until the world settles down, many in our supply chain will be buckling down." John S. Ondik, founder of The Ondik Group, a management consulting firm in Pennsylvania, concurred, observing that "Macro challenges (domestic and global) are driving uncertainty, which impacts planning, hiring, investment – and morale."

Neil Shah, president and CEO of the Construction Financial Management Association (CFMA), identified policy uncertainty as a significant risk. "The uncertainty in policy leading to fluctuations in workforce and inflation are the biggest risk to our business," Shah commented, highlighting the detrimental impact of unpredictable governmental actions on business planning and operational stability.

Geopolitical Tensions Cast a Shadow

The lingering conflict in the Middle East has emerged as a significant factor influencing CEO sentiment, particularly concerning investment and hiring decisions. An increase in the proportion of CEOs planning reductions in capital expenditures and hiring was noted earlier in the year, coinciding with the initial U.S. actions against Iran. The resumption of hostilities during the July survey fielding period, coupled with President Trump’s announcement regarding the end of the Iran cease-fire, has further amplified these concerns.

Geopolitical considerations have become more prominent on CEOs’ radar. However, responses received after the announcement did not reveal a marked increase in negativity. In fact, CEOs’ year-ahead forecasts ticked up slightly from 5.9 among those who responded prior to the announcement to 6.0 among those who responded afterward. What did change significantly was the language used by CEOs to articulate their outlook. War and geopolitical concerns were mentioned in 38 percent of responses received post-announcement, a substantial increase from 24 percent pre-announcement, even though these concerns did not derail the overall forecast trajectory.

The impact of geopolitical events appears to be bifurcated based on a company’s operational footprint. Among CEOs operating solely within the U.S., the year-ahead outlook actually improved from 5.9 to 6.2 after the announcement. In contrast, those with international exposure saw their outlook tick down slightly from 5.9 to 5.8. Even for internationally exposed CEOs, this shift was not dramatic, with their outlook remaining close to neutral or slightly positive. The share of these CEOs expecting conditions to worsen saw a modest uptick, rising from 23 percent to 30 percent.

This divergence underscores the localized impact of global events. One CEO advised a broader perspective, stating, "Watch global economics, because they impact SMB and midsized companies a lot more than you think they do." This sentiment suggests that even domestically focused businesses are not immune to the ripple effects of international instability, whether through supply chain disruptions, currency fluctuations, or shifts in global demand.

The current environment, characterized by a delicate balance of demand strength against pervasive cost pressures, policy ambiguity, and geopolitical instability, is compelling American business leaders to adopt a more cautious and adaptive approach to their strategic planning. While the present business conditions are viewed favorably, the path forward is perceived as fraught with challenges, necessitating a focus on operational resilience, technological innovation, and a keen awareness of evolving global dynamics. The "challenging times" are not merely a fleeting sentiment but a recognized operational reality shaping the decisions of corporate America.