Chief Executive’s latest poll reveals a complex landscape for business leaders, with a notable uptick in CEO confidence juxtaposed against escalating worries about a potential economic downturn. While overall sentiment for current and future business conditions has seen a modest improvement, the undercurrent of economic uncertainty, exacerbated by geopolitical events and persistent inflation, is shaping strategic outlooks for the remainder of 2026.

The Chief Executive CEO Confidence Index registered a 2 percent increase in April, reaching 5.5 out of a possible 10. This marks a return to the index’s starting point for the year, signifying a stabilization of executive sentiment. However, it remains 8 percent below its 12-month peak of 6.0, achieved in December, indicating that the recovery in confidence is still in its nascent stages.

More encouragingly, forward-looking expectations for the next 12 months saw a more substantial 3 percent rise in April, attaining their highest point for 2026. Despite this positive trajectory, the forward-looking index is still 4 percent shy of its 12-month high. Significantly, it now outpaces the assessment of current conditions by a notable 10 percent, suggesting a degree of optimism about the future that is not entirely mirrored in the present operational environment.

This nuanced outlook is further illuminated by the distribution of CEO sentiment. The proportion of leaders anticipating improving business conditions this year climbed to 52 percent in April, a modest increase from 48 percent in March. Concurrently, however, the share of CEOs forecasting a deterioration in economic conditions also grew, rising to 22 percent from 19 percent in the preceding month. This divergence highlights a growing polarization in executive thinking, with a clearer division emerging between those who see a path to growth and those bracing for headwinds.

The decline in the percentage of CEOs expecting stagnant economic conditions—falling to 26 percent in April from 33 percent in March—underscores this polarization. It suggests that business leaders are increasingly taking a definitive stance on the economy’s direction, moving away from a wait-and-see approach.

Geopolitical Tensions and Unforeseen Factors Shape Executive Concerns

The volatile global landscape continues to cast a long shadow over corporate decision-making. One CEO, speaking anonymously, articulated the immense pressure: "The uncontrollable factors facing our organization are at the highest level in my career by many magnitudes. Tariffs, war, energy are creating conditions which require rapid assessment without over-reaction." This sentiment encapsulates the challenge of navigating a business environment marked by interconnected crises.

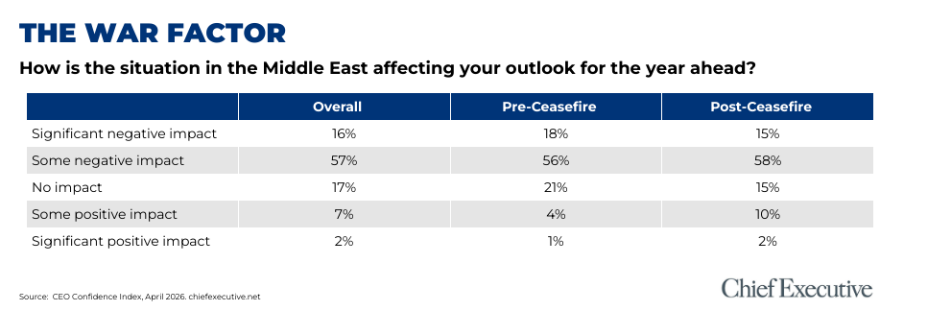

The conflict in the Middle East has emerged as a particularly salient concern. Nearly three-quarters of CEOs reported that the situation is negatively impacting their outlook, with over 40 percent identifying it as a key driver of their current sentiment. While responses submitted after the announcement of a ceasefire indicated a slight improvement in sentiment, the overall level of concern surrounding the conflict has remained remarkably consistent, underscoring its enduring influence on strategic planning. This suggests that the immediate aftermath of the conflict may offer a brief respite, but the underlying instability and its potential for escalation continue to loom large.

Economic Forecasts: Shifting Sands of Growth and Slowdown

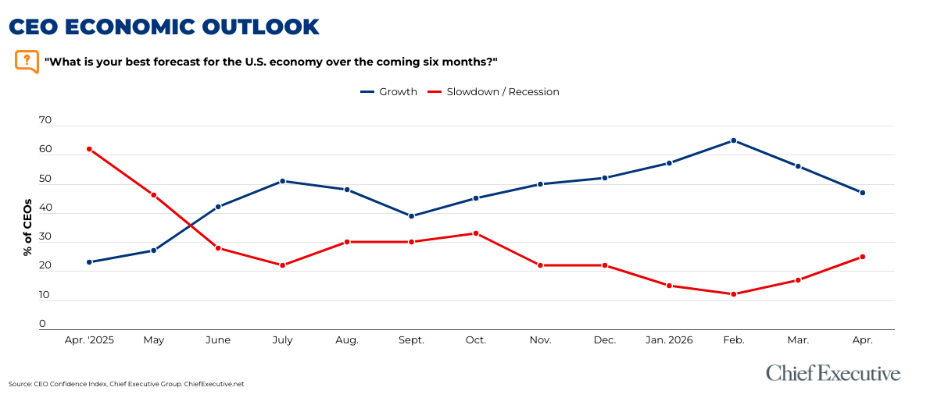

While the majority of CEOs still anticipate near-term growth for the U.S. economy, the pace of that expansion is being recalibrated. The share of executives forecasting growth dipped to 47 percent in April, a noticeable decline from 56 percent in March. Conversely, expectations for an economic slowdown or recession have intensified. Twenty-five percent of CEOs now project a recession or slowdown within the next six months, a significant increase from 17 percent in the previous month. This shift in economic forecasting indicates a growing apprehension about the sustainability of current growth trajectories.

The specter of inflation also continues to trouble business leaders, with forecasts for consumer price increases moving upward. CEOs now anticipate an average 12-month Headline Consumer Price Index (CPI) rate of 4.6 percent, a considerable jump from 3.5 percent in March. This average, while potentially skewed by outliers, is supported by the median inflation expectation, which rose from 3.0 percent in both February and March to 3.3 percent in April. This sustained increase in inflation expectations poses a direct challenge to corporate profitability and consumer purchasing power, necessitating careful management of costs and pricing strategies.

Corporate Outlooks: Revenue, Profits, and Hiring Adjustments

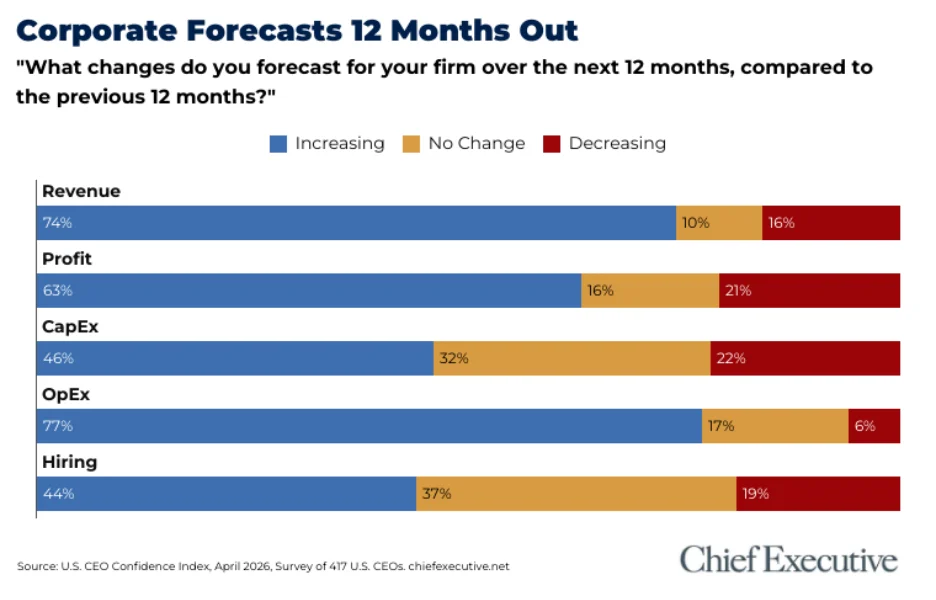

These macroeconomic shifts are directly translating into revised corporate forecasts. Expectations for revenue growth have seen a slight dip, with 74 percent of CEOs anticipating increases, down from 76 percent in March. Similarly, profit growth expectations have softened, with 63 percent of leaders expecting higher profits, a decrease from 66 percent. These modest declines suggest a more cautious approach to top-line and bottom-line performance.

Hiring plans have also been adjusted downward. After showing improvement in March, the percentage of CEOs expecting to increase headcount in 2026 has fallen to 44 percent, a notable drop from 52 percent in the preceding month. This indicates that amidst economic uncertainty and potential slowdowns, companies are exercising greater restraint in expanding their workforces.

In contrast, cost pressures remain a dominant theme. A significant 77 percent of CEOs anticipate rising costs in 2026, reflecting ongoing challenges across various sectors, from supply chain disruptions to labor expenses and raw material prices. This persistent cost inflation will likely necessitate ongoing efforts to optimize operational efficiency and manage expenditures.

Despite these headwinds, a notable degree of investment remains on the horizon. Approximately half of the respondents indicated plans to increase capital expenditures. This suggests that, even in a more uncertain economic climate, a substantial portion of business leaders are committed to investing in their operations, technology, and long-term growth initiatives. This investment may be targeted towards enhancing productivity, bolstering resilience, or capitalizing on emerging opportunities that are less sensitive to short-term economic fluctuations.

Contextualizing the Shift: From Post-Pandemic Recovery to Economic Prudence

The current economic sentiment among CEOs can be understood within the broader context of the post-pandemic recovery. Following a period of significant disruption, businesses experienced a rebound in demand and a surge in growth as economies reopened. This led to a period of heightened optimism and ambitious expansion plans. However, several factors have since converged to temper this optimism.

The lingering effects of supply chain bottlenecks, coupled with the inflationary pressures ignited by strong consumer demand and supply constraints, have created a complex operating environment. Furthermore, the geopolitical landscape has become increasingly volatile, with conflicts and trade tensions introducing new layers of uncertainty. The war in Ukraine, and more recently the conflict in the Middle East, have had ripple effects on energy prices, global trade routes, and overall market stability.

This confluence of factors—persistent inflation, geopolitical instability, and the potential for a global economic slowdown—has prompted a recalibration of executive outlooks. The shift from expecting robust growth to anticipating more moderate expansion and a heightened risk of recession reflects a growing emphasis on resilience, risk management, and strategic prudence.

Analyst Perspectives and Future Implications

Economic analysts are closely monitoring these trends. Some suggest that the increased caution among CEOs is a healthy sign of economic maturity, moving away from an overheated recovery phase towards a more sustainable growth trajectory. Others express concern that the rising pessimism could become a self-fulfilling prophecy, leading to reduced investment and hiring that could indeed trigger a slowdown.

The implications of this evolving CEO sentiment are far-reaching. For consumers, a more cautious corporate environment could translate into slower wage growth, less aggressive hiring, and potentially higher prices if cost pressures persist. For investors, the shift in outlook may lead to a greater focus on companies with strong balance sheets, resilient business models, and clear strategies for navigating economic uncertainty.

For policymakers, the data underscores the ongoing need to address inflation without stifling economic growth. Strategies aimed at easing supply chain pressures, fostering energy independence, and de-escalating geopolitical tensions will be crucial in shaping the economic landscape for the remainder of 2026 and beyond. The coming months will be critical in determining whether the current improvement in CEO confidence is a signal of sustained recovery or a temporary pause before a more significant economic recalibration. The dual presence of cautious optimism and palpable concern paints a picture of an executive class that is both adaptable and increasingly aware of the multifaceted challenges ahead.