Many U.S. manufacturers are recalibrating their economic outlooks, marking an end to a sustained period of positive forecasting that began in February 2026. This shift comes as rising oil prices and escalating international instability cast a lengthening shadow over the sector, prompting a more cautious approach to assessing both current business conditions and future prospects. The latest Chief Executive CEO Confidence Index Survey reveals a notable moderation in sentiment, reflecting a growing unease among industry leaders about the confluence of geopolitical tensions and inflationary pressures.

A Shift from Unwavering Optimism to Cautious Moderation

February and March of 2026 witnessed an unexpectedly buoyant sentiment among U.S. manufacturers. Despite burgeoning geopolitical volatility and a developing global supply crisis, confidence within the sector showed a steady upward trajectory. This period of optimism, however, has now given way to a more subdued outlook. The persistent stressors of international conflict and escalating prices have finally begun to weigh on manufacturers’ perceptions of the business environment.

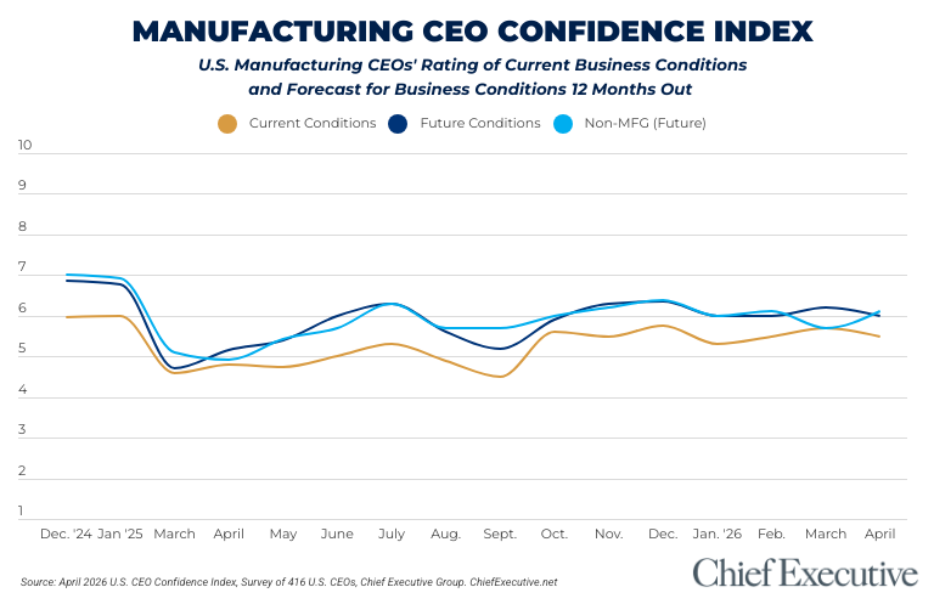

The April 2026 Chief Executive CEO Confidence Index Survey, conducted between April 7th and 9th among 416 U.S. CEOs, indicates this moderation. Manufacturers currently rate their business conditions at an average of 5.5 out of 10, a score that mirrors figures from February 2026. While this represents a 4 percent dip from March’s ratings, it remains a more optimistic assessment than at the beginning of the year, when the index stood at 5.3 out of 10.

Looking ahead, manufacturers anticipate a modest improvement in business conditions over the next 12 months, projecting an increase to 6.0 out of 10 by this time next year. This future forecast, while down 3 percent from March, largely aligns with the expectations held during the first two months of 2026. This suggests a prevailing belief that while current headwinds are significant, a gradual recovery or stabilization is still on the horizon.

Divergent Trends: Manufacturers vs. Non-Manufacturers

Interestingly, the non-manufacturing sector has exhibited a different trend. In April, non-manufacturers maintained their current business condition ratings at a steady 5.5 out of 10. More notably, their future forecasts saw a 3 percent increase from March, even when confronted with the same set of global stressors that are tempering the optimism of their manufacturing counterparts. This divergence highlights sector-specific vulnerabilities and resilience in the face of economic uncertainty.

Key Drivers of Manufacturer Sentiment: Geopolitics and Consumer Behavior

When pressed to elaborate on the factors shaping their economic forecasts, U.S. manufacturers consistently pointed to two primary drivers: the supply chain ramifications of global instability and evolving consumer behavior.

The escalating cost of fuel has emerged as a particularly salient concern. John W. Gessert, CEO of American Plastic Toys, a mid-sized consumer manufacturing firm based in Michigan, articulated this sentiment, stating, "Geopolitics and the increased cost of energy is and will continue to have a negative impact on virtually all aspects of the economy." This viewpoint underscores the pervasive influence of energy prices, not only on production costs but also on broader economic activity.

Echoing this concern, Chris Highfield, President of Pennant Moldings, a family-owned industrial manufacturing firm, highlighted the dual pressure of rising fuel costs and a discernible decrease in consumer spending. He noted that "uncertainty with the Iranian conflict" and "rising costs driven by fuel pricing and [a] reduction of disposable income as consumers spend less" are integral to his firm’s cautious projection. This sentiment suggests a ripple effect from global events to domestic consumer wallets, impacting demand for manufactured goods.

Beyond direct cost pressures, a significant challenge for manufacturers lies in the difficulty of long-term strategic planning amidst such turbulent conditions. Peter Ensch, CEO of Sani-Matic, a large-sized manufacturing firm with international operations, expressed this frustration: "There continues to be too much uncertainty, largely driven by the current administration’s changes in direction, tariff/trade policy and geopolitics that make it very difficult to develop and implement longer term planning." This points to the disruptive impact of policy shifts and geopolitical maneuverings on corporate investment and strategic development.

Geopolitics as a Unifying Concern

A notable shift in the landscape of manufacturer concerns is the increased consensus around geopolitical factors. Unlike previous months, where CEOs might have been broadly categorized by their focus on long-term versus short-term goals, April saw a significant convergence. Nearly three-quarters of manufacturing CEOs cited geopolitics in some regard, solidifying it as a core and unifying issue for the sector. This shared concern suggests that the interconnectedness of global events is now a primary lens through which manufacturers are evaluating their business environment.

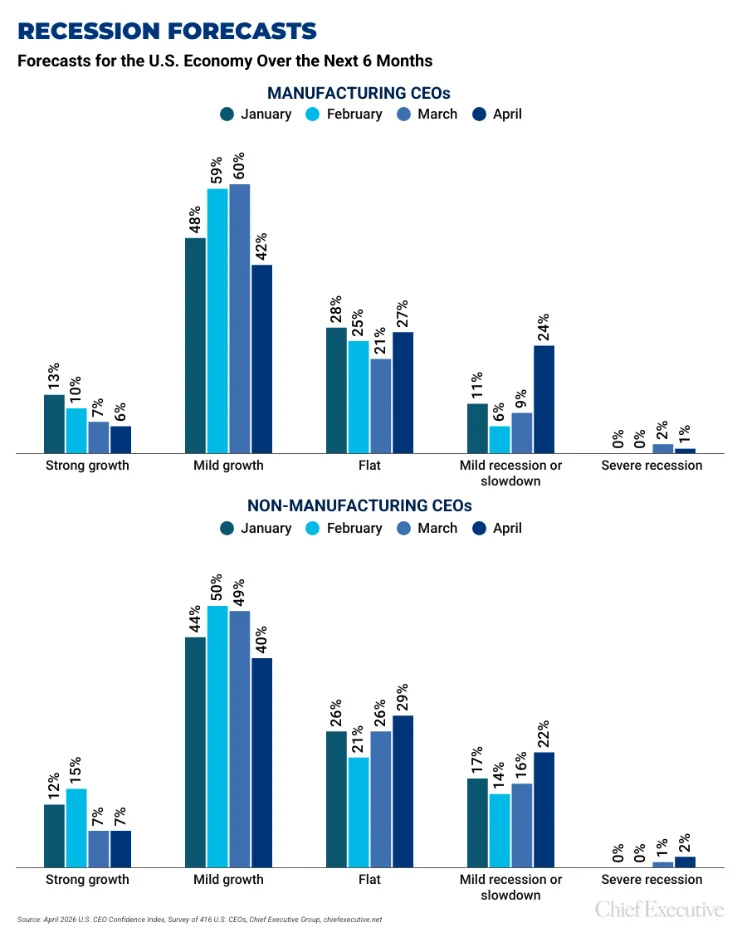

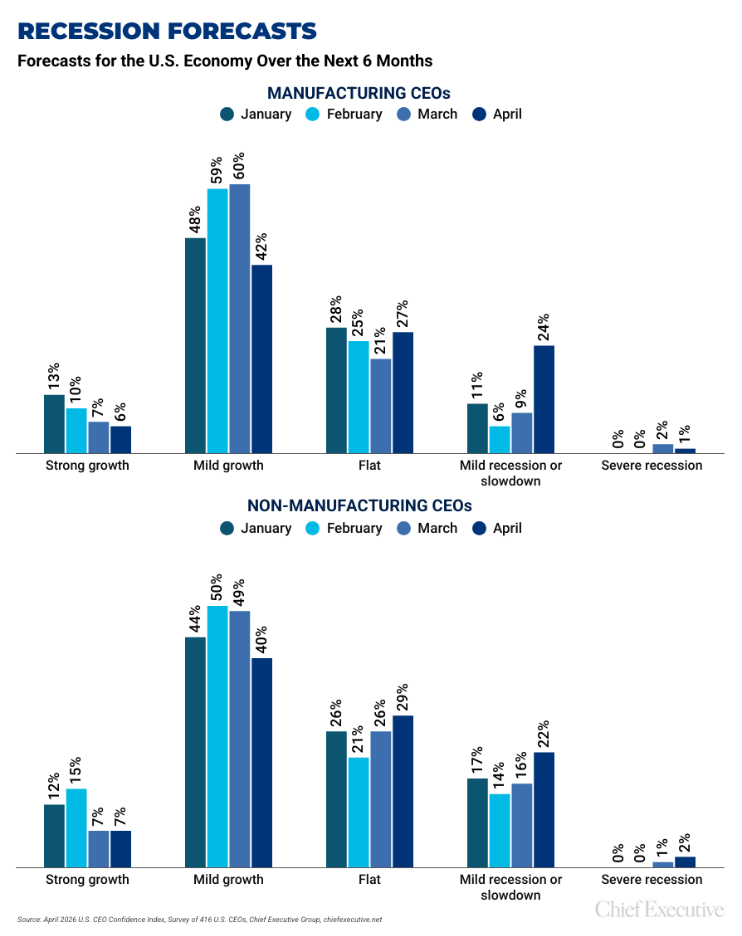

Recession Fears Surge, Growth Projections Dip

The survey results also reveal a stark increase in recessionary fears among manufacturers. In April, 25 percent of manufacturers anticipate some form of recession within the next six months. This represents a staggering 127 percent surge compared to March, when only 11 percent held such concerns.

In tandem with this rise in recessionary sentiment, the proportion of manufacturers projecting overall business growth has declined. This figure dropped from 67 percent in March to just 48 percent in April. Despite this significant decrease, it is important to note that a majority still maintain a positive outlook, suggesting that the current mood reflects a moderation in response to immediate stressors rather than an outright collapse of confidence.

Sectoral Nuances: Consumer vs. Industrial Manufacturing

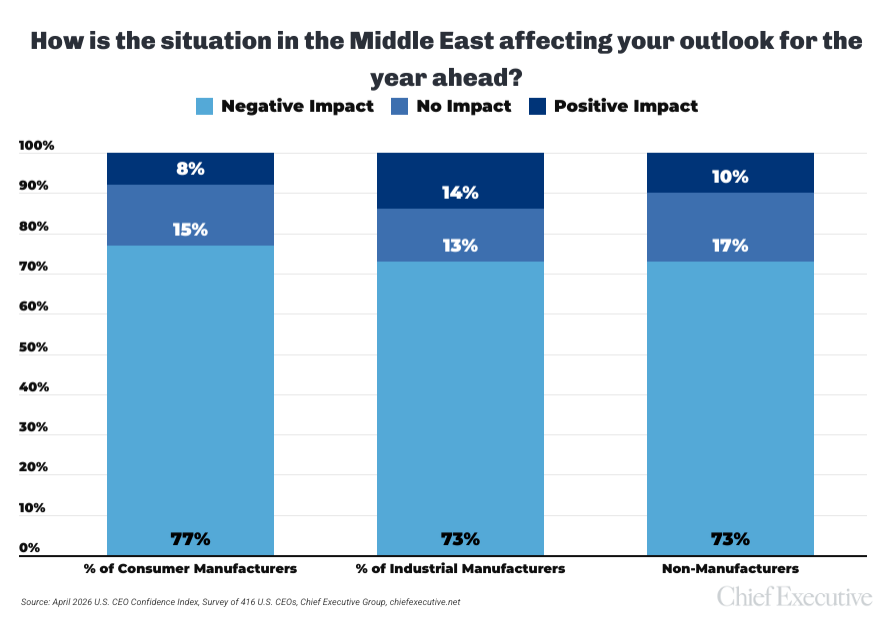

Digging deeper into the impact of the situation in the Middle East, a subtle divide emerges between consumer and industrial manufacturers. A slightly higher percentage of consumer manufacturers (77 percent) reported negative impacts from geopolitical volatility in the region, compared to 73 percent of their industrial-focused peers. While geopolitical instability is a core concern for both groups, the longer production cycles and business-to-business (B2B) structure of many industrial manufacturers may be providing them with a degree of insulation from the immediate turbulence compared to the more direct consumer demand fluctuations faced by consumer-focused firms.

Investment in Capital Expenditures Shows Resilience

Amidst the general moderation in outlook, one area has shown remarkable resilience and even growth: capital expenditures. The percentage of manufacturers planning to increase their capital expenditures saw a significant jump this month, rising by 65 percent. Currently, 86 percent of manufacturers plan to increase capital expenditures, a substantial increase from just 52 percent in March.

This counter-trend could signal a strategic shift within the manufacturing sector. As firms navigate an uncertain landscape, they may be prioritizing investment in internal development and infrastructure to enhance efficiency, build resilience, and position themselves for future growth. This investment could be a proactive measure to mitigate supply chain risks, adopt new technologies, or expand production capacity to meet anticipated future demand, even amidst current cautiousness.

Context and Background: A Volatile Global Environment

The shift in manufacturer sentiment is occurring against a backdrop of significant global events that have been unfolding throughout late 2025 and early 2026. The ongoing conflict in Eastern Europe, which began in early 2022, has continued to disrupt global energy markets and supply chains. This has led to persistent inflationary pressures worldwide, forcing central banks to consider or implement tighter monetary policies.

In addition to the long-standing geopolitical tensions, new flashpoints have emerged, particularly in the Middle East. Escalations in regional conflicts have directly impacted oil production and transportation routes, leading to sharp increases in crude oil prices. This volatility in energy markets has a cascading effect on industries that rely heavily on transportation and energy-intensive manufacturing processes.

Furthermore, trade policies and the ongoing recalibration of international trade relationships have added another layer of complexity. Concerns about tariffs, trade disputes, and the potential for supply chain disruptions due to protectionist measures have created an environment of uncertainty for businesses engaged in international commerce.

Broader Implications for the U.S. Economy

The tempered optimism among U.S. manufacturers carries several important implications for the broader U.S. economy. A slowdown in manufacturing sentiment can translate into reduced hiring, decreased investment in new technologies, and a more cautious approach to expansion. This could potentially dampen overall economic growth and consumer spending.

The rise in recessionary fears is particularly concerning. If a significant portion of manufacturers begin to pull back on production and investment, it could create a self-fulfilling prophecy, leading to a broader economic contraction. The increased focus on capital expenditure, however, offers a glimmer of hope. If these investments are strategic and lead to enhanced productivity and innovation, they could help the sector weather the current storm and emerge stronger.

The divergence between manufacturers and non-manufacturers also warrants attention. The resilience shown by the non-manufacturing sector, particularly in its future outlook, could be a sign of its ability to adapt to changing economic conditions. However, a sustained slowdown in manufacturing, a key engine of job creation and economic output, could eventually impact other sectors as well.

Official Responses and Market Reactions

While the Chief Executive CEO Confidence Index Survey provides a pulse on manufacturer sentiment, official responses from government bodies and central banks are crucial in shaping the economic landscape. The Federal Reserve, for instance, has been closely monitoring inflation and economic growth. Any signs of a significant downturn in key sectors like manufacturing could influence their decisions regarding interest rates and monetary policy.

Market reactions to these trends are also noteworthy. Stock markets often react to shifts in corporate confidence, with declines in manufacturing outlook potentially leading to downward pressure on related equities. Conversely, increased investment in capital expenditures might be viewed positively by investors, signaling a commitment to long-term value creation.

Conclusion: Navigating a Complex Economic Terrain

The latest survey data paints a picture of U.S. manufacturers navigating a complex and increasingly challenging economic terrain. While the sustained optimism of early 2026 has receded, replaced by a more cautious outlook, the sector is not succumbing to outright pessimism. The rise in recessionary fears is a significant concern, but the continued commitment to capital expenditure suggests a strategic intent to build resilience and prepare for future opportunities. The coming months will be critical in determining whether these investments and a degree of underlying optimism can help the manufacturing sector weather the storm of rising energy costs and global instability, or if the moderating expectations will herald a more significant economic slowdown. The interplay of geopolitical events, energy prices, consumer behavior, and policy responses will continue to shape this crucial segment of the U.S. economy.